Table of Contents

In 2017, I made one of the smartest financial decisions of my life — and I almost did not make it. I had just started earning ₹28,000 a month. After rent, groceries, and the mandatory family contribution, I was left with roughly ₹6,000. A colleague told me to start a SIP of ₹5,000 in a Nifty 50 index fund. My first reaction? ‘What is ₹5,000 going to do? That is one dinner at a decent restaurant.’

He said something I will never forget: ‘You are not investing ₹5,000. You are planting a seed that will grow for the next 30 years — even while you sleep.’ I did not fully understand it then. But I set up the auto-debit anyway. Eight years later, that ₹5,000/month SIP — which I have since increased to ₹15,000 — has grown into a corpus that genuinely surprises me every time I check. The invested amount: ₹7.2 lakhs. Current value: ₹14.6 lakhs. I have not done anything smart. I have not timed the market. I have not picked multi-baggers. I simply let compounding do what it does.

If you have read the 50-30-20 Rule, Emergency Funds and the Rule of 72, you are ready for the concept that ties all of personal finance together — the power of compounding. This blog will explain it with real numbers, real Indian examples, and zero jargon. Let us get into it.

What Is the Power of Compounding?

The power of compounding is the process where the returns you earn on an investment start generating their own returns over time. In simple terms: you earn interest on your interest. Your money makes money, and then that money makes more money — creating an accelerating snowball effect that grows exponentially the longer you stay invested.

Albert Einstein reportedly called compound interest ‘the eighth wonder of the world,’ adding: ‘He who understands it, earns it; he who doesn’t, pays it.’ Whether or not Einstein actually said this is debated — but the mathematical reality is not. Compounding is the single most powerful force in personal finance, and it is available to everyone — regardless of income level.

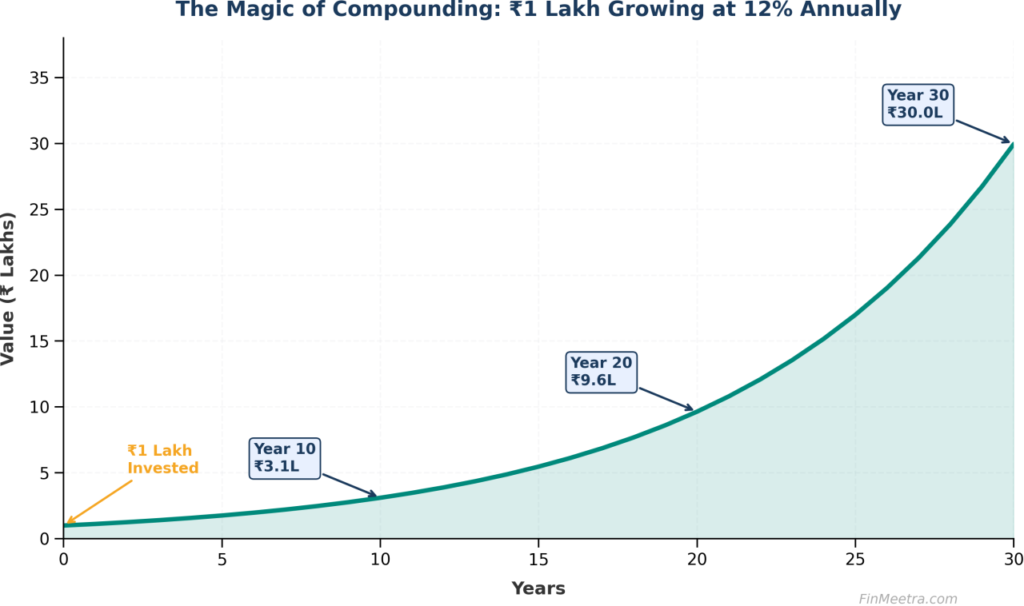

Here is what ₹1,00,000 looks like as it compounds at 12% annually:

| Year | Opening Balance | Interest Earned (12%) | Closing Balance |

| 1 | ₹1,00,000 | ₹12,000 | ₹1,12,000 |

| 2 | ₹1,12,000 | ₹13,440 | ₹1,25,440 |

| 3 | ₹1,25,440 | ₹15,053 | ₹1,40,493 |

| 5 | ₹1,57,352 | ₹18,882 | ₹1,76,234 |

| 10 | ₹2,77,308 | ₹33,277 | ₹3,10,585 |

| 20 | ₹9,64,629 | ₹1,15,755 | ₹10,80,385 |

| 30 | ₹29,95,992 | ₹3,59,519 | ₹33,55,511 |

Notice: In Year 1, you earned ₹12,000. By Year 30, you are earning ₹3.59 lakhs PER YEAR — from the same ₹1 lakh investment. You did nothing extra. Time and compounding did all the heavy lifting.

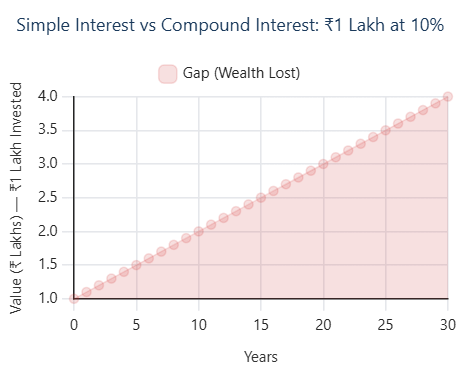

Simple Interest vs. Compound Interest: Why the Difference Is Massive

Most of us learned simple interest in school: Principal × Rate × Time. It is linear — your returns stay flat every year. Compound interest is exponential — your returns grow on top of previous returns. The difference looks small in the first few years but becomes staggering over time.

| Year | Simple Interest (₹1L at 10%) | Compound Interest (₹1L at 10%) | Difference |

| 5 | ₹1,50,000 | ₹1,61,051 | ₹11,051 |

| 10 | ₹2,00,000 | ₹2,59,374 | ₹59,374 |

| 15 | ₹2,50,000 | ₹4,17,725 | ₹1,67,725 |

| 20 | ₹3,00,000 | ₹6,72,750 | ₹3,72,750 |

| 25 | ₹3,50,000 | ₹10,83,471 | ₹7,33,471 |

| 30 | ₹4,00,000 | ₹17,44,940 | ₹13,44,940 |

After 30 years, simple interest gives you ₹4 lakhs. Compound interest gives you ₹17.4 lakhs. The extra ₹13.4 lakhs came from one thing: earning returns on your returns. This is why every financial expert says — never withdraw your returns. Let them reinvest and compound.

The Compounding Formula — Explained Simply

The standard compound interest formula is: A = P × (1 + r/n)^(n × t)

| Symbol | What It Means | Example |

| A | Future value of the investment | What your money grows to |

| P | Principal — initial amount invested | ₹1,00,000 |

| r | Annual interest rate (as a decimal) | 12% = 0.12 |

| n | Times interest compounds per year | 1 (annually), 12 (monthly) |

| t | Number of years | 20 years |

Example: ₹1,00,000 invested at 12% compounded annually for 20 years: A = 1,00,000 × (1.12)^20 = 1,00,000 × 9.6463 = ₹9,64,629. Your ₹1 lakh becomes ₹9.6 lakhs — without adding a single extra rupee.

Understanding the formula helps you appreciate why time (t) is the most powerful variable — doubling t has a far bigger impact than doubling P.

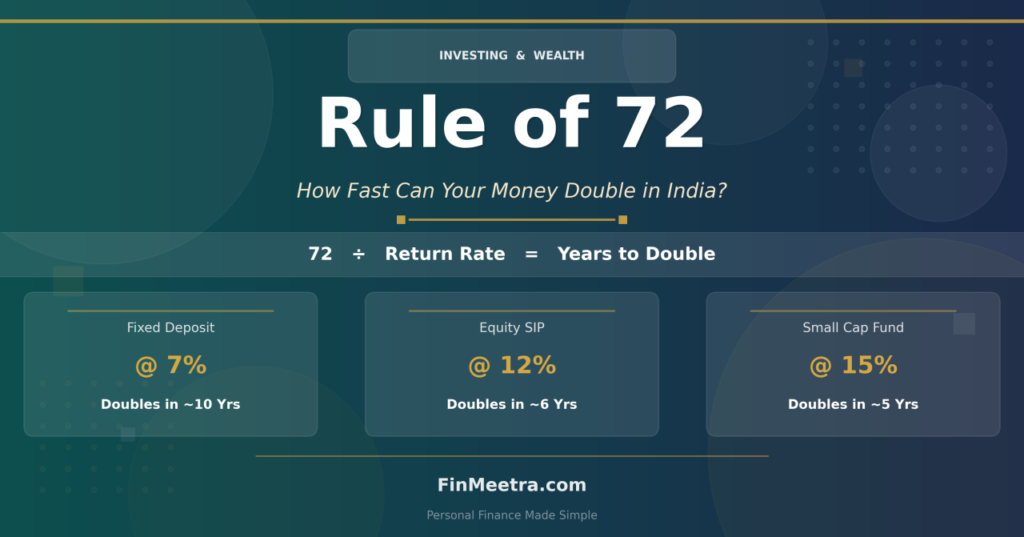

The Rule of 72: Quick Mental Math for Compounding

In Rule of 72, we covered the simplest shortcut for compounding calculations. Quick refresher: divide 72 by your annual return rate to estimate how many years it takes to double your money.

| Annual Return | Years to Double | Real-World Example |

| 6% (FD after tax) | 12 years | ₹5L → ₹10L in 12 years |

| 7.1% (PPF) | ~10 years | ₹5L → ₹10L in ~10 years |

| 8.25% (EPF) | ~9 years | ₹5L → ₹10L in ~9 years |

| 10% (Balanced fund) | 7.2 years | ₹5L → ₹10L in ~7 years |

| 12% (Nifty 50) | 6 years | ₹5L → ₹10L in 6 years |

| 15% (Quality equity) | 4.8 years | ₹5L → ₹10L in ~5 years |

The difference between 6% and 12% seems small annually. But over 30 years, ₹1 lakh at 6% becomes ₹5.7 lakhs while ₹1 lakh at 12% becomes ₹29.96 lakhs — more than 5x as much. This is exactly why equity investments (historically 12%+) dramatically outperform FDs (6-7%) over long periods.

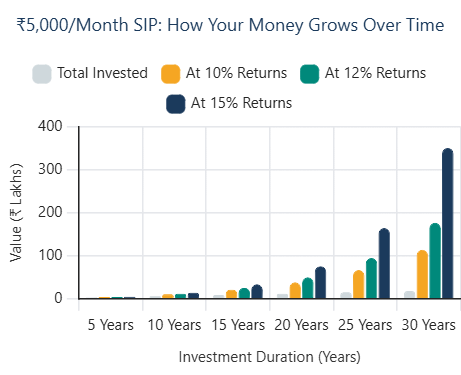

Real Numbers: What ₹5,000/Month SIP Actually Becomes

Forget theory. Here is exactly what a ₹5,000/month SIP looks like at different return rates:

| Duration | Total Invested | Value at 10% | Value at 12% | Value at 15% |

| 5 years | ₹3,00,000 | ₹3,88,685 | ₹4,12,432 | ₹4,48,319 |

| 10 years | ₹6,00,000 | ₹10,24,815 | ₹11,61,695 | ₹13,93,286 |

| 15 years | ₹9,00,000 | ₹20,92,684 | ₹25,24,991 | ₹33,80,768 |

| 20 years | ₹12,00,000 | ₹38,28,485 | ₹49,95,740 | ₹75,79,773 |

| 25 years | ₹15,00,000 | ₹66,49,804 | ₹94,87,726 | ₹1,64,20,449 |

| 30 years | ₹18,00,000 | ₹1,13,02,366 | ₹1,76,49,569 | ₹3,50,49,103 |

Read that last row again: ₹5,000/month for 30 years. You invested only ₹18 lakhs. At 12% returns, you have ₹1.76 crores. At 15%, you have ₹3.5 crores. The remaining ₹1.58 crores (at 12%) is PURE compound interest.

Now imagine you increase your SIP by just 10% every year as your salary grows (₹5,000 → ₹5,500 → ₹6,050…). That ₹1.76 crore becomes over ₹5 crores. This is called a Step-Up SIP, and it is the closest thing to a wealth hack in personal finance.

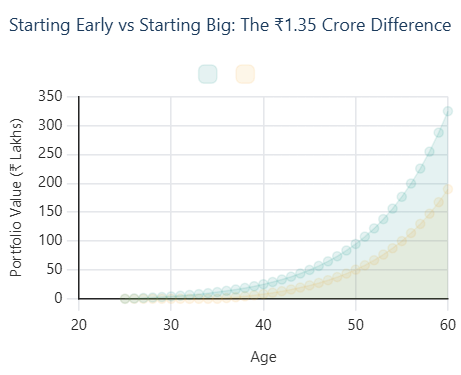

The Tale of Two Friends: Why Starting Early Beats Starting Big

This is the story I tell everyone who says ‘I will start investing next year.’

| Parameter | Ajay (Starts at 25) | Vikram (Starts at 35) |

| Monthly SIP | ₹5,000 | ₹10,000 |

| Investment Period | 25 → 60 = 35 years | 35 → 60 = 25 years |

| Annual Returns | 12% | 12% |

| Total Invested | ₹21,00,000 | ₹30,00,000 |

| Corpus at Age 60 | ₹3,24,74,402 | ₹1,89,76,378 |

| Wealth Gained | ₹3,03,74,402 | ₹1,59,76,378 |

Vikram invests DOUBLE the amount every month, invests ₹9 lakhs MORE in total — and STILL ends up with ₹1.35 crores LESS than Ajay. Why? Because Ajay gave his money 10 extra years to compound. Those 10 years are worth more than ₹9 lakhs of additional capital.

The practical implication: if you are reading this at age 30, the second-best time to start investing is today. Every year of delay has a real, measurable, permanent cost to your final wealth.

Where Compounding Works Best in India

| Investment | Avg Returns | Tax Treatment | Lock-in | Best For |

| Equity MF (SIP) | 10-14% | LTCG >₹1.25L at 12.5% | None (ELSS: 3yr) | Long-term wealth |

| PPF | 7.1% | EEE (fully exempt) | 15 years | Conservative + tax saving |

| EPF | 8.25% | EEE (if 5+ years) | Till retirement | Salaried employees |

| NPS | 9-11% | Partial tax on withdrawal | Till 60 | Retirement + ₹50K extra tax |

| Sukanya Samriddhi | 8.2% | EEE (fully exempt) | 21 years | Girl child planning |

| Fixed Deposit | 6.5-7.5% | Taxed at slab rate | Flexible | Short-term / emergency |

Key insight: PPF, EPF, and Sukanya Samriddhi enjoy EEE status (Exempt-Exempt-Exempt) — meaning no tax when you invest, no tax on growth, and no tax when you withdraw. A 7.1% PPF return with zero tax actually beats a 9% FD return taxed at 30% (effective: 6.3%).

Where Compounding Works Best in the USA

| Investment | Avg Returns | Tax Treatment | Contribution Limit (2026) | Best For |

| 401(k) | 8-10% | Tax-deferred growth | $23,500/year | Employer-matched retirement |

| Roth IRA | 8-10% | Tax-FREE growth + withdrawal | $7,000/year | Tax-free retirement income |

| S&P 500 Index Fund | 10-11% | LTCG taxed | No limit | Passive wealth building |

| 529 Plan | 6-8% | Tax-free for education | Varies by state | Children’s college fund |

| HSA | 7-9% | Triple tax advantage | $4,300 individual | Medical + retirement |

The 3 Enemies of Compounding (And How to Beat Them)

Compounding is powerful — but fragile. Three things break it consistently:

Enemy #1: Withdrawing Early (Breaking the Chain)

Every time you redeem your investments early, you reset the compounding clock to zero. I made this mistake in 2019 — I withdrew ₹80,000 from my mutual fund to buy a phone I did not need. At 12% compounding, that ₹80,000 would be worth ₹2.5 lakhs in 10 years. I essentially paid ₹2.5 lakhs for a phone now in a drawer.

Enemy #2: Panic Selling During Market Crashes

In March 2020, the Nifty 50 crashed 38% in three weeks. My portfolio showed a ₹1.2 lakh loss. My instinct screamed ‘SELL.’ A colleague said: ‘Your SIP is buying the same units at 38% discount. Why would you stop?’ I held. By December 2020, my portfolio recovered and hit a new high. Those who panic-sold locked in losses permanently.

Enemy #3: High Fees and Unnecessary Taxes

A 1.5% expense ratio vs. 0.2% seems trivial. But over 20 years on ₹10 lakhs at 12%: the 0.2% fund gives ₹93.2 lakhs. The 1.5% fund gives ₹71.4 lakhs. You lost ₹21.8 lakhs to fees. That is not a fee — that is a wealth tax.

Real-Life Problem & Solution

Meera, a 29-year-old HR professional in Hyderabad, earning ₹55,000/month, wanted to start investing but felt she was ‘too late’ and did not have ‘enough money.’ She had ₹12,000 left after expenses but was putting it all in her savings account at 3.5%.

We sat down and built a plan:

| Action | Amount | Expected Return | Value in 20 Years |

| SIP in Nifty 50 Index Fund | ₹5,000/month | 12% | ₹49.96 lakhs |

| PPF (₹1.5L annual) | ₹3,000/month | 7.1% | ₹13.29 lakhs |

| NPS (extra tax saving) | ₹2,000/month | 10% | ₹15.28 lakhs |

| Emergency Fund (liquid fund) | ₹2,000/month | 6.5% | Built in 18 months → redirected |

| TOTAL | ₹12,000/month | — | ₹78.53 lakhs+ (conservative) |

Meera’s ₹12,000/month — money she was keeping in a savings account earning ₹420/month in interest — will grow to nearly ₹80 lakhs in 20 years. If she increases her SIP by 10% annually, she is looking at ₹1.5+ crores. She is not a high earner. She is not a stock market expert. She is simply someone who understood compounding and started.

She told me three months later: ‘The SIP auto-debits on the 5th. I do not even notice it. But seeing my Groww portfolio slowly grow — that feeling is addictive in the best way.’

Compounding Beyond Money: The Most Underrated Life Hack

Here is what most finance blogs will not tell you: compounding does not just work with money. It works with anything where small, consistent effort accumulates over time.

| Area | Small Daily Input | Compounding Effect Over 5 Years |

| Fitness | 30 minutes of walking | 50+ kg weight difference vs. sedentary lifestyle |

| Reading | 20 pages/day | 365+ books — top 1% in your field |

| Career Skills | 1 hour of learning | Expert-level mastery in 2-3 new skills |

| Relationships | 15 minutes of quality time | Deeper trust, stronger bonds |

| Writing/Content | 500 words/day | 3-4 published books or 500+ blog posts |

I started this blog because I wrote 200 words a day for 6 months. It compounded. Compounding is not just a financial concept — it is a life philosophy.

Pro Tips to Maximize Compounding in Your Financial Life

- Start TODAY — not next month, not next year. The best time was 10 years ago. The second-best time is right now.

- Automate your investments — set up SIP auto-debit on salary day. What you do not see, you do not spend.

- Never withdraw for wants — maintain a separate emergency fund so you never break investments.

- Increase SIP by 10% every year — a step-up SIP can 3x your final corpus compared to a flat SIP.

- Choose growth option over dividend — reinvesting returns keeps the compounding chain intact.

- Review annually, not daily — checking daily creates anxiety. Once a year is enough.

- Use the Rule of 72 — divide 72 by your return rate to know when your money doubles.

Frequently Asked Questions About the Power of Compounding

Q: What is the power of compounding in simple terms?

A: The power of compounding means your investment returns generate their own returns over time. Instead of earning interest only on your original amount, you earn interest on your original amount PLUS all the interest you have already earned. Over long periods, this creates exponential growth — turning small regular investments into significant wealth.

Q: How much will ₹5,000/month SIP grow in 20 years?

A: At 12% annual returns (approximate historical Nifty 50 returns), ₹5,000/month SIP for 20 years grows to approximately ₹49.96 lakhs. Your total investment is ₹12 lakhs — the remaining ₹37.96 lakhs is pure compound interest. At 15%, it grows to approximately ₹75.8 lakhs.

Q: Does compounding work in fixed deposits?

A: Yes, FDs do compound — typically quarterly. However, FD interest is taxed at your income slab rate, which significantly reduces the effective compounding rate. A 7% FD for someone in the 30% tax bracket effectively earns only ~4.9% after tax — barely beating inflation.

Q: Is it too late to start investing at 35 or 40?

A: It is never too late — but it gets more expensive with every year of delay. If you start at 35 instead of 25, you need to invest roughly 2-3x more monthly to reach the same corpus at retirement. The key is to start immediately with whatever amount you can afford.

Q: What is the difference between the Rule of 72 and compounding?

A: The Rule of 72 is a quick mental shortcut derived from the compounding formula. Divide 72 by your annual return rate to estimate how many years it takes to double your money. For example, at 12% returns, your money doubles every 6 years (72 ÷ 12 = 6).

Related Articles You’ll Love

- #1: The 50-30-20 Rule — The Simplest Budgeting Framework That Actually Works

- #2: Emergency Funds — How Much You Really Need and Where to Keep It

- #3: The Rule of 72 — The Mental Math Shortcut Every Investor Should Know

Key Takeaways

- Compounding means earning returns on your returns — the single most powerful force in personal finance.

- ₹5,000/month at 12% for 30 years = ₹1.76 crores (you invested only ₹18 lakhs).

- Starting 10 years earlier beats investing double the amount — time is more valuable than money.

- The 3 enemies of compounding: early withdrawal, panic selling, and high fees.

- Use tax-free compounding vehicles (PPF, EPF, Sukanya Samriddhi, Roth IRA) for maximum effect.

- Compounding works beyond money — apply it to health, skills, relationships, and career.

- The best time to start was yesterday. The second-best time is RIGHT NOW.

────────────────────────────────────────────────────────────

📩 ENJOYED THIS BLOG? HERE IS WHAT YOU CAN DO NEXT:

- 💬 Leave a Comment — Tell me: at what age did you start investing? And what is your current SIP amount? I read every comment.

- 📧 Subscribe to the FinMeetra Newsletter — Get new blog posts, free calculators, and exclusive money tips delivered to your inbox every week.

- 📊 Download Free SIP Compounding Calculator — Plug in your SIP amount, expected returns, and number of years to see exactly how your money will grow.

- 📱 Share This Blog — If this helped you, share it with someone who needs to see these numbers. WhatsApp, LinkedIn, Twitter — your choice.

Pingback: How to Start Your First SIP in India — Complete 2026 Guide | FinMeetra

Pingback: Free SIP Calculator Excel: 8-Sheet Premium Toolkit (2026) | FinMeetra

Pingback: Index Funds vs Active Funds: Which Wins for Indian's 2026? | FinMeetra

Pingback: 90% Indians Own the Wrong Mutual Fund Category | FinMeetra

Pingback: I Tracked My SIP for 10 Years: The Hidden Truth (2026) | FinMeetra

Pingback: The ₹50 Lakh Trap: Why Most Indians Retire Poor Despite Earning Well | FinMeetra

Pingback: Rent vs Buy House in India: The 30-Year Math That Costs You ₹3 Crore (2026) | FinMeetra