Table of Contents

I remember the exact moment I almost did not start investing.

It was October 2017. I had just received my second salary — ₹28,000. After rent, groceries, and the mandatory family transfer, I had about ₹6,000 left. A colleague at work — the same one who later convinced me to start a Nifty 50 SIP (Read Power of Compounding) — said something that stuck: ‘Just start a SIP of ₹500. You will not miss it. But in 10 years, you will thank yourself.’ My first reaction was embarrassment. ₹500? That felt like nothing. What could ₹500 possibly do? I almost did not set it up. But that evening, out of curiosity more than conviction, I downloaded an app, completed my KYC in 10 minutes, and started a ₹500 SIP in a Nifty 50 index fund. No research. No analysis. Just ₹500 and a leap of faith.

That ₹500 SIP was the single best financial decision I have ever made — not because of the returns (though those have been great), but because it broke the mental barrier. Once I saw that first auto-debit go through painlessly, I increased it to ₹1,000, then ₹2,000, then ₹5,000. Today, eight years later, I invest ₹15,000/month across three funds — and my total portfolio has crossed ₹14.6 lakhs from a total investment of ₹7.2 lakhs.

If you have read the 50-30-20 Rule, Emergency Funds, the Rule of 72, and the Power of Compounding, you already have the foundation. This blog is the action step — how to actually start your first SIP in India, step by step, in 2026. No jargon. No complicated terms. Just a clear, practical guide that even your parents will understand. Let us get into it.

What Is SIP (Systematic Investment Plan)?

A Systematic Investment Plan (SIP) is a method of investing a fixed amount of money into a mutual fund scheme at regular intervals — typically monthly. Instead of investing a large lump sum at once, SIP allows you to invest small amounts (₹100 to ₹1,00,000+) every month, automatically deducted from your bank account on a date you choose. Think of SIP as a recurring deposit — but instead of earning 5-6% in a bank, your money is professionally managed and invested in stocks, bonds, or both, with historically higher returns of 10-15% over the long term.

SIP is not a product — it is a method. You do not ‘buy a SIP.’ You invest in a mutual fund through SIP mode. The mutual fund is the vehicle; SIP is the fuel delivery system that keeps it running every month without you having to think about it.

| SIP Feature | What It Means | Example |

| Systematic | Fixed amount, fixed date, every month | ₹5,000 on the 5th of every month |

| Investment | Money goes into a mutual fund (equity/debt/hybrid) | Nifty 50 Index Fund |

| Plan | Auto-debit from bank — no manual action needed | Set once, runs for years automatically |

| Minimum Amount | As low as ₹100-₹500 per month | SEBI Chhoti SIP: ₹250 |

| Flexibility | Pause, increase, decrease, or stop anytime | No lock-in (except ELSS: 3 years) |

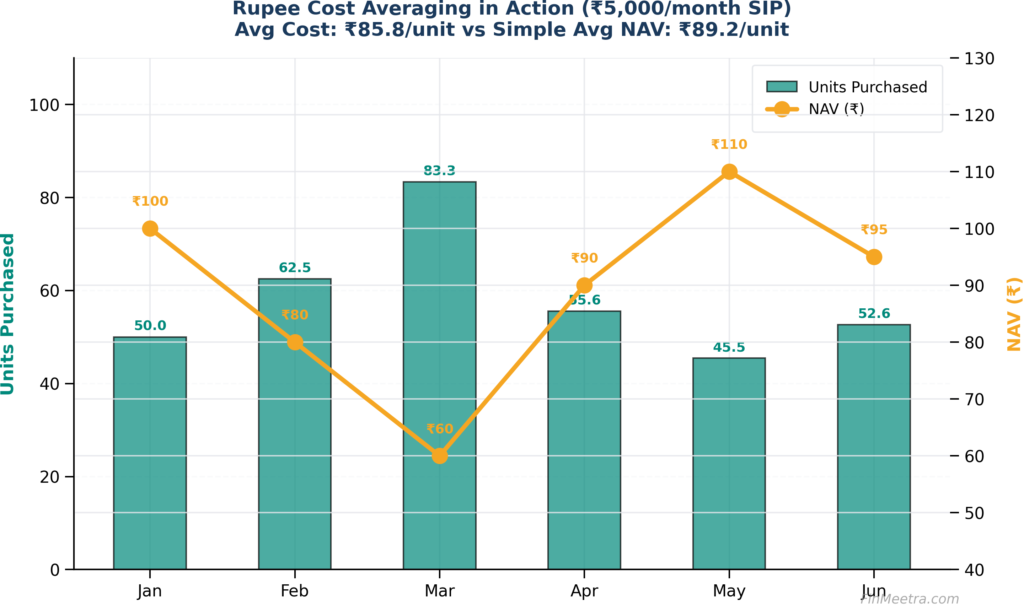

How SIP Works: The Magic of Rupee Cost Averaging

Rupee Cost Averaging is the single biggest advantage of SIP over lump sum investing. When you invest a fixed amount every month, you automatically buy more units when the market is down (prices are cheap) and fewer units when the market is up (prices are expensive). Over time, this averages out your cost per unit — often lower than the average market price.

Here is a real example: imagine you invest ₹5,000/month in a mutual fund whose NAV (Net Asset Value) fluctuates over 6 months:

| Month | NAV (₹) | SIP Amount | Units Purchased |

| January | ₹100 | ₹5,000 | 50.0 |

| February | ₹80 | ₹5,000 | 62.5 |

| March | ₹60 | ₹5,000 | 83.3 |

| April | ₹90 | ₹5,000 | 55.6 |

| May | ₹110 | ₹5,000 | 45.5 |

| June | ₹95 | ₹5,000 | 52.6 |

| TOTAL | Avg NAV: ₹89.2 | ₹30,000 | 349.5 units |

Your average cost per unit: ₹30,000 ÷ 349.5 = ₹85.8. The simple average NAV was ₹89.2. You saved ₹3.4 per unit — automatically, without any market timing. This is why SIP investors often outperform lump sum investors in volatile markets. The months when the market crashed (March at ₹60) were actually your best months — you bought the most units at the cheapest price.

The 3 Superpowers of SIP

Superpower #1: Compounding (Interest on Interest)

In The Power of Compounding, we showed how ₹5,000/month at 12% for 30 years grows to ₹1.76 crores — from just ₹18 lakhs invested. SIP is the delivery mechanism that feeds compounding consistently. Every month, your SIP adds fresh fuel to the compounding engine. The longer you stay invested, the more powerful it becomes.

Superpower #2: Rupee Cost Averaging (Buy Low Automatically)

As we just covered, SIP automatically buys more units when markets fall and fewer when markets rise. This removes the impossible task of ‘timing the market’ — something even professional fund managers struggle with. You do not need to know whether the market is high or low. Your SIP handles it.

Superpower #3: Discipline (The Invisible Advantage)

The hardest part of investing is not picking the right fund. It is staying consistent. SIP automates this — the money leaves your account before you can spend it. In the 50-30-20 Rule, we recommended allocating 20% of income to savings and investments. SIP is how you actually execute that 20% allocation without willpower.

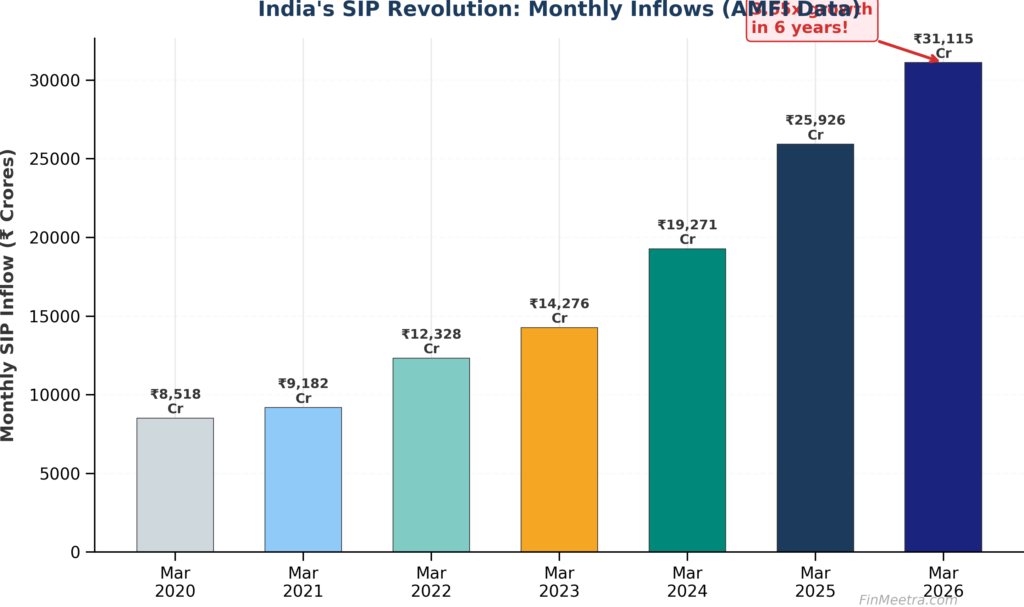

India’s SIP Revolution: The Numbers Don’t Lie

India is in the middle of an unprecedented SIP revolution. According to AMFI (Association of Mutual Funds in India), monthly SIP inflows hit ₹31,115 crores in April 2026 — up from just ₹8,518 crores in March 2020. That is a 3.65x increase in just 6 years. There are now over 10.44 crore active SIP accounts in India, and the total mutual fund industry AUM stands at ₹81.92 lakh crores. SIP is no longer a niche investment strategy — it is mainstream India’s preferred way to build wealth.

| Period | Monthly SIP Inflow | Active SIP Accounts | Key Milestone |

| March 2020 | ₹8,518 Cr | ~3.1 Cr | COVID crash — SIPs continued |

| March 2021 | ₹9,182 Cr | ~3.9 Cr | Post-COVID recovery rally |

| March 2022 | ₹12,328 Cr | ~5.3 Cr | Crossed ₹10,000 Cr milestone |

| March 2023 | ₹14,276 Cr | ~6.4 Cr | Steady growth despite global uncertainty |

| March 2024 | ₹19,271 Cr | ~8.4 Cr | Crossed ₹15,000 Cr → ₹19,000 Cr |

| March 2025 | ₹25,926 Cr | ~9.3 Cr | Crossed ₹25,000 Cr milestone |

| April 2026 | ₹31,115 Cr | 10.44 Cr | Record high! 3.65x growth in 6 years |

The practical takeaway: if over 10 crore Indians are investing through SIP every month, you are not early — you are on time. And the numbers prove that SIP investors stayed during COVID (March 2020), during the Russia-Ukraine war (2022), and during every market correction since. Discipline wins.

How Much Should You Invest? SIP Amount Guide by Salary

The most common question beginners ask is: ‘How much should I invest in SIP?’ The answer depends on your salary, expenses, and existing commitments. Here is a practical guide based on the 50-30-20 Rule:

| Monthly Salary | Recommended SIP | % of Salary | Suggested Allocation |

| ₹15,000 | ₹1,500-2,000 | 10-13% | ₹1,500 Nifty 50 Index Fund |

| ₹25,000 | ₹3,000-5,000 | 12-20% | ₹3,000 Index + ₹2,000 ELSS |

| ₹40,000 | ₹5,000-8,000 | 13-20% | ₹5,000 Index + ₹3,000 Flexi Cap |

| ₹60,000 | ₹8,000-12,000 | 13-20% | ₹6,000 Index + ₹3,000 ELSS + ₹3,000 Flexi Cap |

| ₹1,00,000 | ₹15,000-20,000 | 15-20% | ₹8,000 Index + ₹5,000 Flexi + ₹4,000 ELSS + ₹3,000 NPS |

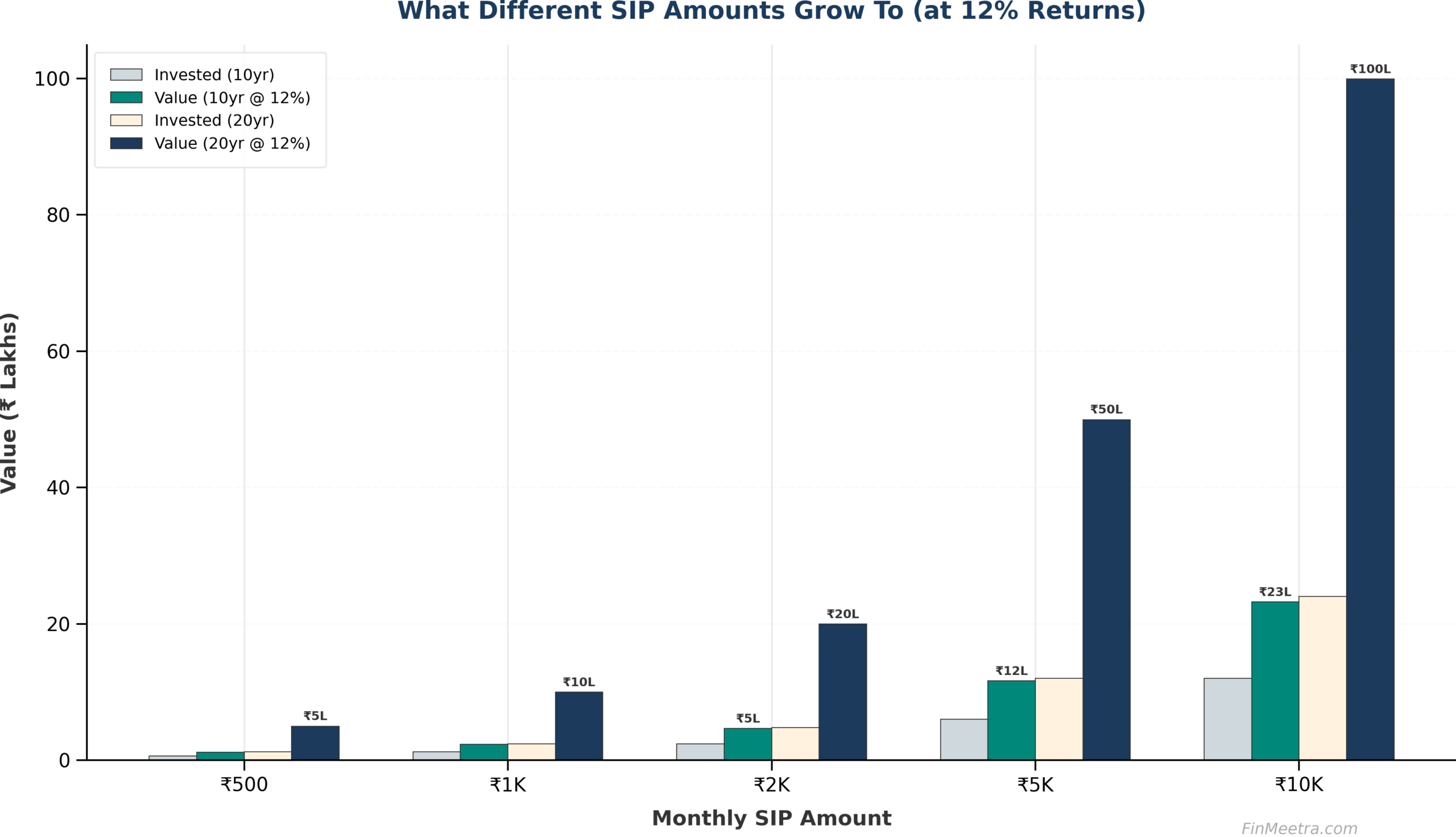

Key principle: start with what is comfortable, not what is impressive. A ₹500 SIP that you maintain for 20 years is infinitely more valuable than a ₹10,000 SIP that you stop after 6 months because it felt like too much. Start small, build the habit, then increase.

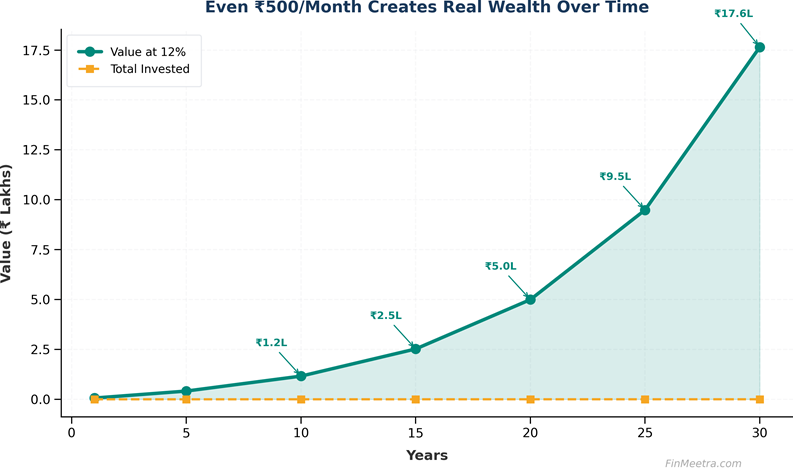

Even ₹500/Month Creates Real Wealth

If you think ₹500 is too small to make a difference, look at these numbers. This table shows what ₹500/month SIP becomes at 12% annual returns (approximate Nifty 50 long-term returns):

| Duration | Total Invested | Value at 12% | Wealth Gained | Return Multiple |

| 5 years | ₹30,000 | ₹41,243 | ₹11,243 | 1.37x |

| 10 years | ₹60,000 | ₹1,16,170 | ₹56,170 | 1.94x |

| 15 years | ₹90,000 | ₹2,52,499 | ₹1,62,499 | 2.81x |

| 20 years | ₹1,20,000 | ₹4,99,574 | ₹3,79,574 | 4.16x |

| 25 years | ₹1,50,000 | ₹9,48,773 | ₹7,98,773 | 6.33x |

| 30 years | ₹1,80,000 | ₹17,64,957 | ₹15,84,957 | 9.81x |

Read that last row: ₹500/month for 30 years. You invested ₹1.8 lakhs. Your portfolio is worth ₹17.6 lakhs. The remaining ₹15.8 lakhs is pure compound interest. You did not do anything clever. You just did not stop. Now imagine if you had started with ₹5,000/month — that final number becomes ₹1.76 crores.

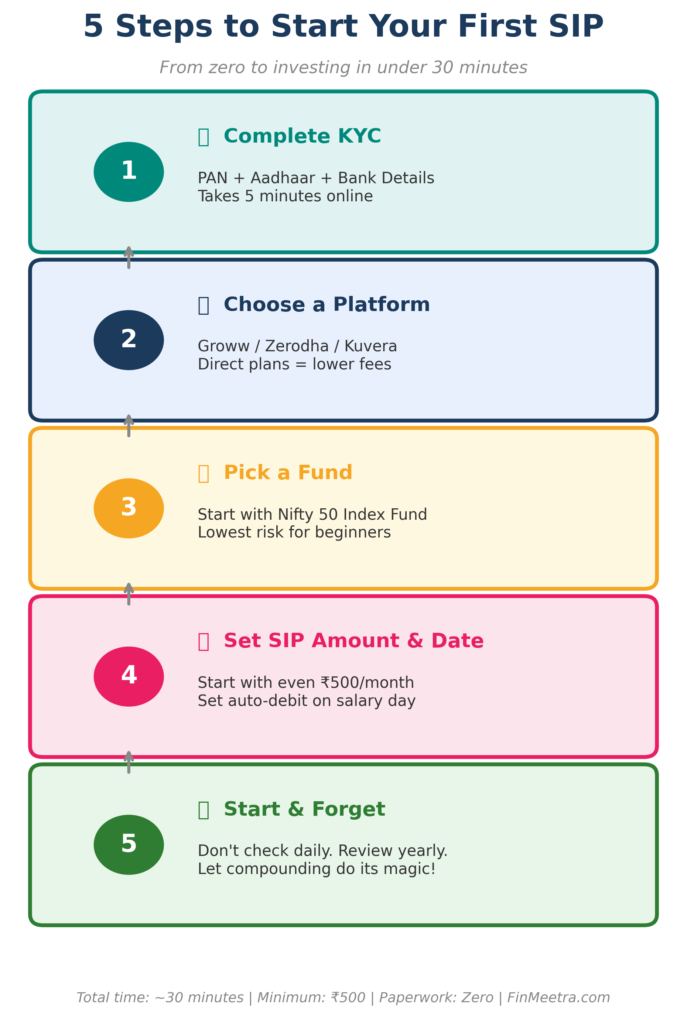

5 Steps to Start Your First SIP Today

Let us break down each step in detail:

Step 1: Complete Your KYC (Know Your Customer)

KYC is a one-time process required by SEBI for all mutual fund investors in India. You need: PAN card, Aadhaar card, and a bank account with auto-debit facility. Most platforms offer eKYC — fully online, completed in 2-10 minutes using Aadhaar OTP. No physical paperwork required.

Step 2: Choose a Platform

| Platform | Direct Plans | Min SIP | Key Feature | Best For |

| Groww | ✅ Yes | ₹100 | Simplest UI, beginner-friendly | First-time investors |

| Zerodha Coin | ✅ Yes | ₹100 | Demat-based, advanced tools | Stock + MF investors |

| Kuvera | ✅ Yes | ₹100 | Goal-based, tax harvesting | Tax-conscious investors |

| PayTM Money | ✅ Yes | ₹100 | UPI auto-pay, familiar app | PayTM ecosystem users |

| ET Money | ✅ Yes | ₹100 | Expense tracking + investing | All-in-one finance users |

Important: Always choose Direct Plans, not Regular Plans. Direct Plans have lower expense ratios (0.1-0.5% vs 1-2%) because they cut out the distributor commission. Over 20 years, this difference can be ₹10-20 lakhs on a ₹5,000/month SIP.

Step 3: Pick Your Fund

For absolute beginners, the safest and simplest choice is a Nifty 50 Index Fund. It invests in India’s top 50 companies, has the lowest expense ratio (0.1-0.2%), requires zero research, and has historically returned 12-14% over the long term. You can diversify later — but start here.

Step 4: Set SIP Amount & Date

Choose an amount you will not miss. Start with ₹500, ₹1,000, or ₹5,000 — whatever fits your budget after following the 50-30-20 Rule and setting up your Emergency Fund . Set the SIP date to 1-5 days after your salary credit date so the money leaves before you can spend it.

Step 5: Start & Forget

Once your SIP is set up with auto-debit, your job is done. Do not check your portfolio daily. Do not panic when markets crash. Do not redeem for wants. Review once every 6-12 months. Increase your SIP by 10% every year when your salary increases. That is it. Compounding and rupee cost averaging will do the rest.

Best SIP Funds for Beginners in 2026

You do not need 10 funds. For most beginners, 2-3 funds are enough. Here are the five categories to consider:

| Fund Category | Example Funds | Expense Ratio | Risk Level | Best For |

| Nifty 50 Index Fund | UTI Nifty 50, HDFC Nifty 50 | 0.10-0.20% | Moderate | Core holding for ALL beginners |

| Nifty Next 50 Index Fund | ICICI Pru Nifty Next 50, Motilal Oswal | 0.15-0.30% | Moderate-High | Growth-oriented investors |

| Flexi Cap Fund | Parag Parikh, PPFAS, HDFC Flexi Cap | 0.50-1.00% | Moderate-High | Diversified across market caps |

| ELSS (Tax Saving) | Mirae Asset ELSS, Quant ELSS | 0.50-0.80% | Moderate-High | Section 80C tax saving (₹1.5L) |

| Balanced Advantage | ICICI BAF, HDFC BAF | 0.50-1.00% | Low-Moderate | Conservative / first-time investors |

Beginner recommendation: Start with just ONE fund — a Nifty 50 Index Fund. After 6-12 months, once you are comfortable, add a second fund (Flexi Cap or ELSS). Never invest in more than 3-4 funds — overlap reduces diversification benefit.

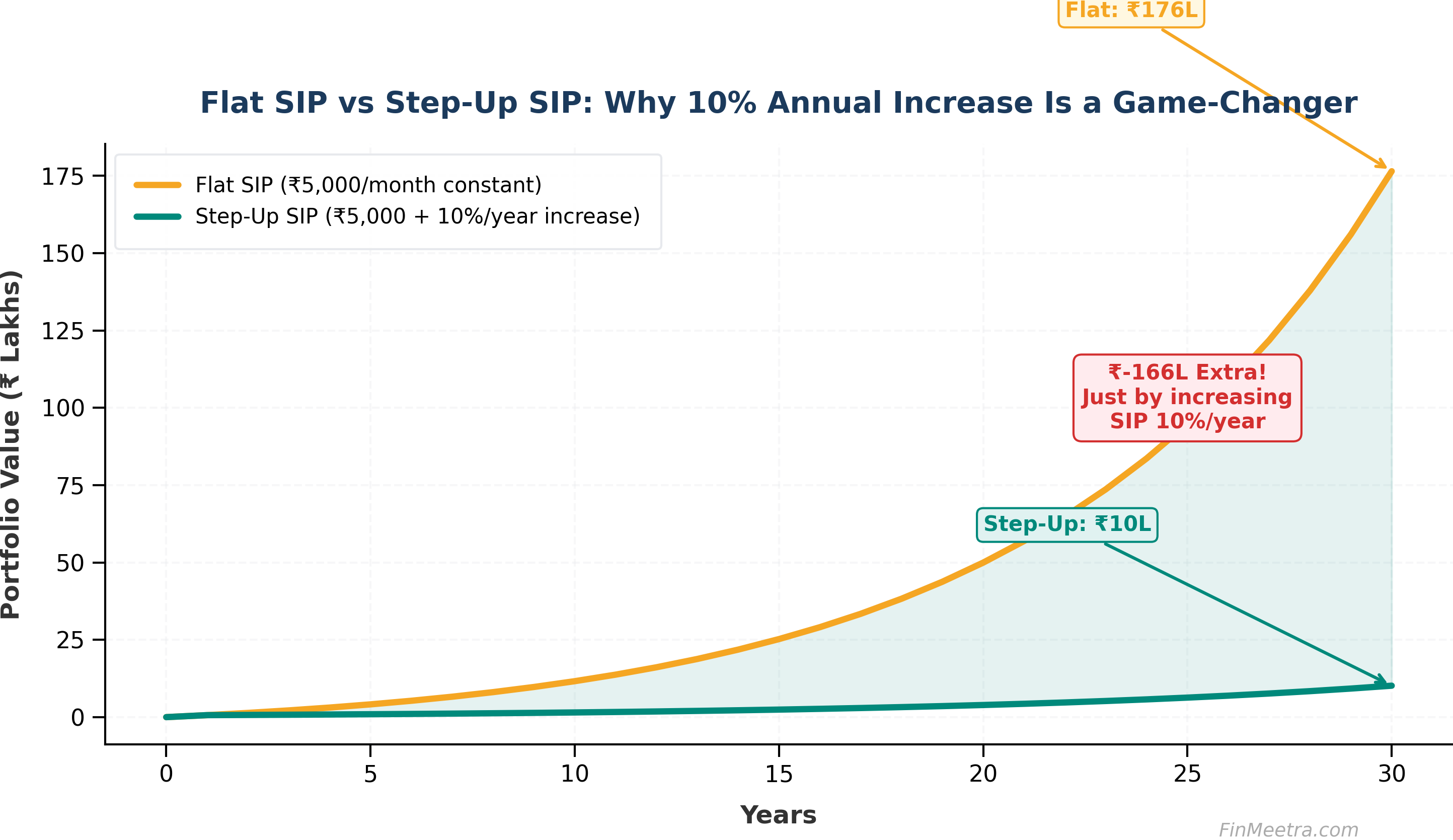

The Step-Up SIP Strategy: How to 3x Your Wealth

A Step-Up SIP (also called Top-Up SIP) is when you increase your SIP amount by a fixed percentage every year — typically 10%, aligned with your annual salary increment. The impact is staggering:

| Duration | Flat SIP (₹5K/month) | Step-Up SIP (₹5K + 10%/yr) | Extra Wealth from Step-Up |

| 10 years | ₹11.6L | ₹16.9L | ₹5.3L |

| 15 years | ₹25.2L | ₹44.2L | ₹19.0L |

| 20 years | ₹49.9L | ₹105.8L | ₹55.9L |

| 25 years | ₹94.9L | ₹239.7L | ₹144.8L |

| 30 years | ₹1.76 Cr | ₹5.34 Cr | ₹3.58 Cr |

The difference is mind-blowing: by simply increasing your SIP by 10% every year (which most salaried professionals can easily do with annual increments), your 30-year corpus jumps from ₹1.76 crores to over ₹5 crores — more than 3x! Most platforms (Groww, Zerodha, Kuvera) allow you to set up automatic Step-Up SIPs.

SIP Taxation in India 2026

Understanding SIP taxation is crucial for maximizing your returns. Each SIP installment is treated as a separate investment for tax purposes:

| Fund Type | Holding Period | Tax Classification | Tax Rate |

| Equity MF (SIP) | Less than 1 year | STCG (Short-Term) | 20% |

| Equity MF (SIP) | More than 1 year | LTCG (Long-Term) | 12.5% above ₹1.25L exemption |

| Debt MF | Any period | Taxed at slab rate | As per your income tax slab |

| ELSS | 3-year lock-in | LTCG | 12.5% above ₹1.25L exemption |

| Hybrid Fund (65%+ equity) | More than 1 year | LTCG | 12.5% above ₹1.25L exemption |

Tax-saving tips: (1) Hold equity SIPs for at least 1 year to qualify for LTCG instead of STCG. (2) Use ELSS SIP for ₹1.5 lakh tax deduction under Section 80C. (3) The ₹1.25 lakh LTCG exemption resets every financial year — plan redemptions across years. (4) Use tax-free instruments like PPF and EPF alongside equity SIPs for a balanced portfolio (Blog #4).

5 Biggest SIP Mistakes Beginners Make (And How to Avoid Them)

Mistake #1: Stopping SIP During Market Crashes

This is the most expensive mistake. In March 2020, the Nifty crashed 38%. Investors who stopped their SIPs locked in losses. Those who continued bought units at a 38% discount. By December 2020, the market recovered and their portfolios hit new highs. Market crashes are SIP’s best friend — they let you accumulate more units at lower prices.

Mistake #2: Choosing Funds Based on Last Year’s Returns

Last year’s topper is rarely next year’s topper. Instead, look for funds with consistent 5-10 year track records, low expense ratios, and stable fund managers. A Nifty 50 Index Fund eliminates this guesswork entirely.

Mistake #3: Starting Too Late (“I’ll start next year”)

Every year of delay has a permanent cost. Starting at 25 vs 35 — even with double the SIP amount at 35 — results in ₹1.35 crores LESS ( Ajay vs Vikram story). The second-best time to start is today.

Mistake #4: Redeeming for Wants Instead of Needs

Breaking a SIP for a vacation, gadget, or wedding outfit resets the compounding clock. This is exactly why Emergency Funds exists — build a 6-month emergency fund FIRST, so you never touch your SIP investments for non-emergencies.

Mistake #5: Not Increasing SIP Annually

A flat ₹5,000 SIP for 30 years gives ₹1.76 crores. A Step-Up SIP (10% annual increase) gives ₹5+ crores. That is 3x more wealth, just by increasing ₹500 per year. Always activate Step-Up SIP.

Real-Life Problem & Solution

Arjun is a 24-year-old software developer in Pune earning ₹30,000/month. After rent (₹8,000), food (₹5,000), family (₹5,000), and miscellaneous (₹4,000), he has ₹8,000 left. He wants to invest but feels overwhelmed by choices. He also has zero emergency fund and student loan EMIs of ₹3,000/month.

We built this plan using the 50-30-20 framework:

| Action | Amount/Month | Expected Return | Value in 15 Years |

| Emergency Fund (Liquid Fund) | ₹2,000 | 6.5% | Built in 12 months → redirected to SIP |

| SIP in Nifty 50 Index Fund | ₹3,000 | 12% | ₹25.2 lakhs |

| ELSS SIP (Tax Saving) | ₹1,500 | 12% | ₹12.6 lakhs |

| PPF (₹18,000/year) | ₹1,500 | 7.1% | ₹5.1 lakhs |

| TOTAL | ₹8,000 | — | ₹42.9 lakhs+ (conservative) |

Arjun’s ₹8,000/month — money he was leaving in a savings account at 3.5% — will grow to nearly ₹43 lakhs in 15 years. When his salary increases, he will activate Step-Up SIP and that corpus could cross ₹1 crore by age 45. He told me: ‘I spent 30 minutes setting it up. Now it runs on autopilot. I wish I had started at 22 instead of 24.’

Frequently Asked Questions About Starting SIP

Q: What is SIP in simple terms?

A: SIP (Systematic Investment Plan) is a method of investing a fixed amount every month in a mutual fund. It is like a recurring deposit but with higher potential returns. Your bank auto-debits the amount, and professional fund managers invest it for you. You can start with as little as ₹100-₹500 per month.

Q: What is the minimum amount to start SIP in India in 2026?

A: Most mutual funds allow SIPs starting at ₹100-₹500 per month. SEBI’s Chhoti SIP initiative allows SIPs from ₹250. Platforms like Groww, Zerodha, and Kuvera support these low-amount SIPs.

Q: Which is the best fund for SIP beginners?

A: For absolute beginners, a Nifty 50 Index Fund is the safest starting point. It tracks India’s top 50 companies, has the lowest expense ratio (0.1-0.2%), requires zero fund research, and has delivered 12-14% annual returns historically over 15+ year periods.

Q: Is SIP better than lump sum investing?

A: For salaried individuals with monthly income, SIP is better because it eliminates market timing risk through rupee cost averaging. For someone with a large windfall (bonus, inheritance), a Systematic Transfer Plan (STP) — which invests lump sum into liquid fund and auto-transfers monthly to equity — is the ideal approach.

Q: Can I stop or pause my SIP anytime?

A: Yes. SIPs can be paused, increased, decreased, or stopped at any time (except ELSS which has a 3-year lock-in per installment). However, stopping SIP during market crashes is the single biggest mistake investors make — it locks in losses and breaks compounding.

Q: How is SIP taxed in India?

A: Equity SIP gains held for less than 1 year are taxed at 20% (STCG). Gains held for more than 1 year are taxed at 12.5% with a ₹1.25 lakh annual exemption (LTCG). Each SIP installment has its own 1-year holding period. ELSS has a mandatory 3-year lock-in.

Q: How do I increase my SIP amount?

A: Most platforms offer a Step-Up SIP (or Top-Up SIP) feature where you can set an automatic annual increase (e.g., 10% per year). You can also manually modify your SIP amount through your platform’s app. We recommend increasing SIP by at least 10% every year with your salary increment.

Related Articles You’ll Love

- The 50-30-20 Rule — The Simplest Budgeting Framework That Actually Works

- Emergency Funds — How Much You Really Need and Where to Keep It

- The Rule of 72 — The Mental Math Shortcut Every Investor Should Know

- The Power of Compounding — How ₹5,000/Month Grows into ₹1.76 Crores

Key Takeaways

- SIP is a method, not a product — it auto-invests a fixed amount monthly into mutual funds via bank auto-debit.

- Rupee Cost Averaging means SIP automatically buys MORE units when markets fall and fewer when markets rise.

- Even ₹500/month at 12% for 30 years grows to ₹17.6 lakhs — you invest only ₹1.8 lakhs.

- India’s SIP inflows crossed ₹31,115 crores/month in April 2026 with 10.44 crore active accounts (AMFI).

- Start with a Nifty 50 Index Fund — lowest cost, zero research, 12-14% historical returns over 15+ years.

- Always choose Direct Plans (0.1-0.5% fees) over Regular Plans (1-2%) — saves ₹10-20L over 20 years.

- Step-Up SIP (10% annual increase) turns ₹1.76 Cr into ₹5+ Cr over 30 years — 3x more wealth.

- The best time to start was 10 years ago. The second-best time is RIGHT NOW. Start with whatever you can.

Pingback: SIP vs Lump Sum: Which Investment Strategy Wins? 2026 | FinMeetra

Pingback: I Tracked My SIP for 10 Years: The Hidden Truth (2026) | FinMeetra

Pingback: PPF vs ELSS vs NPS Calculator: Best 80C Investment for FY 2026-27 | FinMeetra

Pingback: When Will You Become Financially Free? Calculator + Real Indian Roadmap | FinMeetra

Pingback: You Earn ₹20 LPA Salary. Why Doesn't It Feel Like It? (Real Numbers)