Table of Contents

In our earlier guide, we explained how to choose the right mutual fund using a 7-filter framework. But choosing the fund is only half the job. The other half — and honestly, the part most Indians miss — is how much you invest and how that amount grows over time.

Here’s a strange pattern most investors fall into.

They start a SIP at 25 with whatever salary they have. Their salary doubles by 30. Triples by 35. But their SIP? Still the same number from 10 years ago. 😅

That’s the silent reason most people end up with smaller corpuses than they imagined — even after investing “consistently” for years.

The fix is simple. It’s called Step-Up SIP. And once you understand it, you’ll never look at your SIP the same way again.

What Is a Step Up SIP?

A Step-Up SIP (also called Top-Up SIP) is a regular SIP that automatically increases by a fixed percentage every year. So instead of investing the same amount forever, your SIP grows with your income.

Think of it like this:

🟢 Regular SIP: ₹5,000 every month, forever

🚀 Step-Up SIP (10%): ₹5,000 → ₹5,500 → ₹6,050 → ₹6,655 …

A small bump. Once a year. Set and forget.

That’s all. But the impact over 20–25 years is massive.

Why This One Habit Quietly Builds Crores

Let’s break it down with simple math.

If you invest ₹10,000/month for 25 years at 12% return:

| Strategy | Final Wealth |

| 🟢 Regular SIP (₹10K flat) | ₹1.89 Cr |

| 🟡 Step-Up SIP (5% yearly) | ₹2.61 Cr |

| 🟢 Step-Up SIP (10% yearly) | ₹3.65 Cr |

| 🚀 Step-Up SIP (15% yearly) | ₹5.20 Cr |

Same starting SIP. Same return. Same fund.

But almost 3x more wealth, just by growing the SIP a little every year.

This is what most people miss. The fund didn’t change. The market didn’t change. Only the habit changed.

If you ever wondered how compounding actually works in real numbers, Step-Up SIP is compounding on steroids. It compounds both your money and your contribution.

The Real Problem with Flat SIPs

Here’s something most people don’t realise.

When you keep your SIP flat for 10 years, three things quietly happen:

❌ Inflation eats your investment value

A ₹5,000 SIP in 2015 was a big deal. In 2025, it barely buys a weekend brunch.

❌ Your saving rate falls

If your salary doubles but your SIP stays the same, you’re actually saving a smaller % of your income every year.

❌ You miss the compounding upgrade

Every extra rupee invested early compounds for decades. Skipping a yearly step-up is skipping free wealth.

The 50-30-20 budget rule recommends saving 20% of income. But if your SIP doesn’t grow with your salary, your savings rate silently drops below 10% — and you don’t even realise it.

How Much Should You Step-Up Every Year?

There’s no single right answer, but here’s a simple framework based on your stage of life and income:

| Step-Up % | Best For | What It Does |

| 🟢 5% | Conservative investors, low salary growth | Beats inflation |

| 🟢 10% | Most salaried professionals | Matches typical salary hikes |

| 🚀 15% | High earners, aggressive savers | Maximises long-term wealth |

🎯 Rule of thumb: Set your step-up % equal to your average yearly salary hike. That way, your SIP grows naturally with your income — without ever feeling like a sacrifice.

If you don’t have a strong emergency fund in place yet, build that first before chasing aggressive step-ups. Investing without a safety net is risky — no matter how smart the strategy.

Step-Up SIP vs Lump Sum: Which Wins?

This is a common question. The honest answer is — both work, but for different reasons.

A lump sum works when you have a big amount and the market is favourable. A SIP (and especially a Step-Up SIP) works when you want consistency, discipline, and growth tied to your income. We’ve explained this trade-off in detail in our SIP vs Lump Sum guide.

But here’s a simple takeaway:

| Situation | Best Choice |

| You earn a steady salary | ✅ Step-Up SIP |

| You got a one-time bonus | ✅ Lump sum (or STP) |

| You’re a first-time investor | ✅ Step-Up SIP |

| You want zero stress + auto-grow | ✅ Step-Up SIP |

For 90% of salaried Indians, Step-Up SIP is the cleanest, simplest, most powerful path to building long-term wealth.

The Math That Will Change Your Mind

Let’s run a quick reality check.

Here’s the wealth created at different SIP amounts and step-ups (25 years, 12% return):

| Monthly SIP | No Step-Up | 10% Step-Up | Extra Wealth |

| ₹3,000 | ₹57 Lakh | ₹1.09 Cr | +₹52 Lakh |

| ₹5,000 | ₹94 Lakh | ₹1.82 Cr | +₹88 Lakh |

| ₹10,000 | ₹1.89 Cr | ₹3.65 Cr | +₹1.76 Cr |

| ₹15,000 | ₹2.83 Cr | ₹5.47 Cr | +₹2.64 Cr |

| ₹25,000 | ₹4.72 Cr | ₹9.12 Cr | +₹4.40 Cr |

Look at the last column. That’s the wealth you leave on the table by not stepping up your SIP.

Not because you can’t afford to. Just because you never set it up. 💔

How to Set Up a Step-Up SIP in India (Step-by-Step)

The good news? Setting up a Step-Up SIP is easier than ever.

🪜 The 5-Step Setup

Step 1: Log in to your investment platform (Groww, Zerodha Coin, Kuvera, MF Central, or AMC website).

Step 2: Choose your mutual fund.

If you’re unsure how to pick the right one, follow the 7-filter mutual fund framework first.

Step 3: Select Start SIP → enter your monthly amount.

Step 4: Look for the “Step-Up SIP” or “Annual Increase” option → set it to 10% (or your preferred %).

Step 5: Confirm tenure (long-term preferred → 15–25 years). Done. ✅

Most platforms now offer this feature by default. If yours doesn’t, you can manually update your SIP every year on your birthday or salary appraisal month. Simple trick — same outcome. 🎯

If you’re brand new to SIP investing, start with our beginner’s SIP guide before stepping up — first understand the basics, then layer in the smart habits.

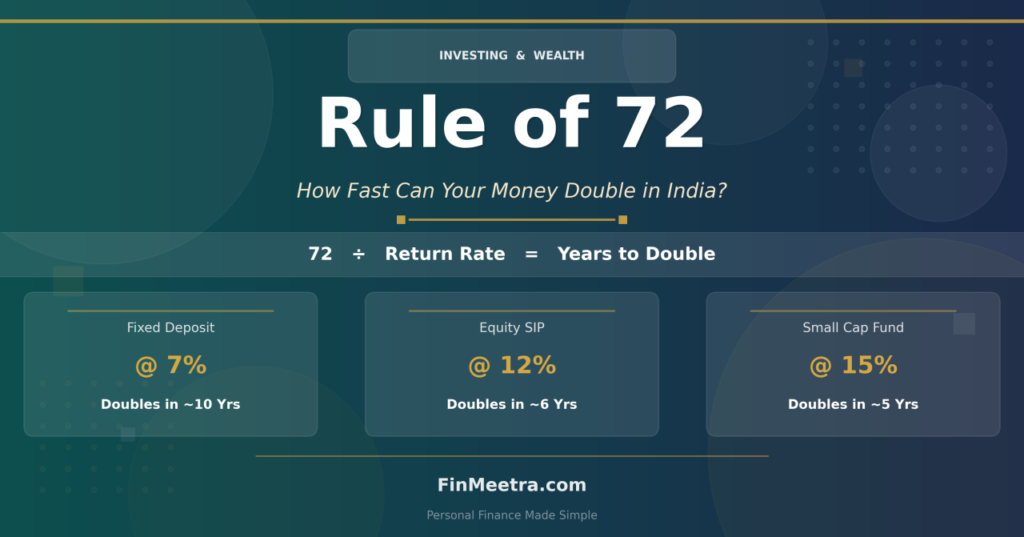

The Hidden Power: Time + Step-Up = Magic

There’s a powerful little math trick that explains all of this.

It’s called the Rule of 72 — how fast money doubles. Combined with a Step-Up SIP, your money doesn’t just double — it doubles faster every cycle, because you’re not just relying on compounding. You’re also feeding it more fuel every year.

This is why a Step-Up SIP works so beautifully:

🚀 Time compounds your old money

🚀 Your salary hikes feed in new money

🚀 Both grow together — quietly, every year

That’s how ordinary salaries quietly turn into extraordinary corpuses.

Common Mistakes to Avoid

Even smart investors fumble Step-Up SIPs. Watch out for these traps:

❌ Setting step-up too low (1–2%) → barely beats inflation

❌ Stopping step-up after 3–4 years → kills the magic

❌ Pausing during market dips → biggest wealth destroyer

❌ Not tracking yearly progress → review every 12 months

❌ Mixing emergency fund into SIP → keep them separate

🎯 The whole point of Step-Up SIP is automation + consistency. Don’t overthink it. Set it. Forget it. Let it grow.

A Simple Story: Raj vs Aman

Let’s bring this to life.

Raj and Aman both started working in 2025 at age 25. Both earn ₹50,000/month. Both decide to invest ₹5,000 in the same mutual fund.

🟢 Raj — sticks to flat ₹5,000 SIP for 25 years.

🚀 Aman — increases his SIP by 10% every year.

Fast forward to 2050:

| Metric | Raj | Aman |

| 💸 Total Invested | ₹15 Lakh | ₹59 Lakh |

| 📈 Final Wealth | ₹94 Lakh | ₹1.82 Cr |

| 💰 Extra Money Earned | — | ₹88 Lakh more |

Raj saved on “effort.”

Aman built almost ₹1 Crore more — without ever feeling the pinch.

That’s the silent power of Step-Up SIP. 🌱

Key Takeaways

✅ A flat SIP is a SIP losing to inflation. Don’t freeze your future.

✅ Step-Up SIP grows your investment with your income — automatically.

✅ Even a 10% yearly step-up can nearly 2x your final wealth.

✅ 5% beats inflation. 10% matches salary growth. 15% builds serious wealth.

✅ Set it once on Groww/Zerodha/Kuvera — let automation do the work.

✅ The earlier you start, the bigger the difference compounds.

✅ Step-Up SIP works because it compounds both money and habit.

✅ Most Indians don’t lose to bad funds. They lose to flat SIPs.

Frequently Asked Questions

Q: What is a Step-Up SIP?

A: A Step-Up SIP is a regular SIP that automatically increases by a fixed percentage every year. Instead of investing the same amount forever, your SIP grows along with your income, helping you build a much larger corpus over time.

Q: How is Step-Up SIP different from a normal SIP?

A: A normal SIP invests the same amount every month for the entire tenure. A Step-Up SIP increases that amount automatically each year — say, by 5%, 10%, or 15% — so it adjusts to your rising income and beats inflation.

Q: Is Step-Up SIP better than a regular SIP?

A: For most salaried Indians, yes. Since your income grows yearly, your SIP should grow too. Even a small 10% yearly step-up can nearly double your final wealth over 25 years compared to a flat SIP.

Q: How much should I step-up my SIP every year?

A: A safe rule is 10%, which matches average salary hikes. If you’re conservative, start with 5%. If you’re aggressive and earn well, go up to 15%. The key is consistency — even small step-ups compound massively.

Q: Can I start a Step-Up SIP on Zerodha, Groww, or Kuvera?

A: Yes. All major platforms in India — Groww, Zerodha Coin, Kuvera, MF Central, and most AMC websites — offer a built-in Step-Up SIP option. You can set it during SIP creation or update it later.

Q: Can I stop or change my Step-Up SIP anytime?

A: Yes. You can pause, stop, or change the step-up % anytime. There are no penalties. But the longer you continue, the more powerful the compounding becomes.

Q: Will Step-Up SIP guarantee higher returns?

A: No SIP guarantees returns since mutual funds are market-linked. But a Step-Up SIP improves your final corpus by simply increasing your investment over time — which is a controllable factor, unlike market returns.

Q: When should I start a Step-Up SIP?

A: The best time is the day you start your first SIP. The second-best time is today. The earlier you start, the more powerful the step-up effect becomes — because both your money and your contribution compound for longer.

Related Articles You’ll Love

The 50-30-20 Rule — The Simplest Budgeting Framework That Actually Works

Emergency Funds — How Much You Really Need and Where to Keep It

The Rule of 72 — How Fast Your Money Can Double

The Power of Compounding — How ₹5,000/Month Grows into ₹1.76 Crores

How to Start Your First SIP in India — Complete Beginner’s Guide

SIP vs Lump Sum — Which Strategy Actually Wins?

How to Choose the Right Mutual Fund — 7-Filter Framework

Free SIP Premium Calculator (Excel)

Pingback: SIP Calculator – Calculate Mutual Fund SIP Returns with Step-Up | FinMeetra