Table of Contents

Rule of 72 – The Conversation That Changed How I Think About Money

(And Why I Wish Someone Told Me This at 22)

A few years ago, during a casual lunch with a senior colleague, I casually mentioned that I had parked ₹2 Lakhs in a savings account “for the time being.” He looked at me, smiled, and asked one simple question:

| “Do you know how many years it will take for that ₹2 Lakhs to become ₹4 Lakhs sitting in your savings account?” |

I did the math later. At 3.5% savings account interest, using the Rule of 72: 72 ÷ 3.5 = roughly 20.5 years. Twenty years. Just to double. Meanwhile, the same money in a decent equity mutual fund at 12% would double in just 6 years.

That single conversation rewired how I looked at every rupee I earned. And today, as a Chartered Accountant who has spent years in corporate finance, I can tell you — the Rule of 72 is the single most underrated mental shortcut in personal finance.

If you have already started budgeting with the 50-30-20 rule and built your emergency fund, this is your next step. Because building wealth is not just about saving — it is about understanding how fast your money actually grows.

Let us break it down — simply, practically, and with real Indian numbers.

What Is the Rule of 72? (And Why Every Indian Should Know It)

The Rule of 72 is a quick, elegant mental shortcut that answers one of the most important questions in personal finance:

| “How many years will it take for my money to double at a given rate of return?” |

Instead of pulling out a compound interest calculator or wrestling with logarithmic formulas, you simply divide 72 by your annual rate of return. That is it. The result tells you the approximate number of years needed for your investment to double.

This rule works because of the mathematical properties of compound interest. The number 72 is derived from the natural logarithm of 2 (approximately 0.693), adjusted for easier mental arithmetic. While it is most accurate for returns between 6% and 10% — which conveniently covers most Indian investment products — it gives a remarkably close approximation even outside this range.

Whether you are a salaried professional, a founder bootstrapping your startup, or a student just getting curious about money — this one formula will change how you evaluate every financial decision.

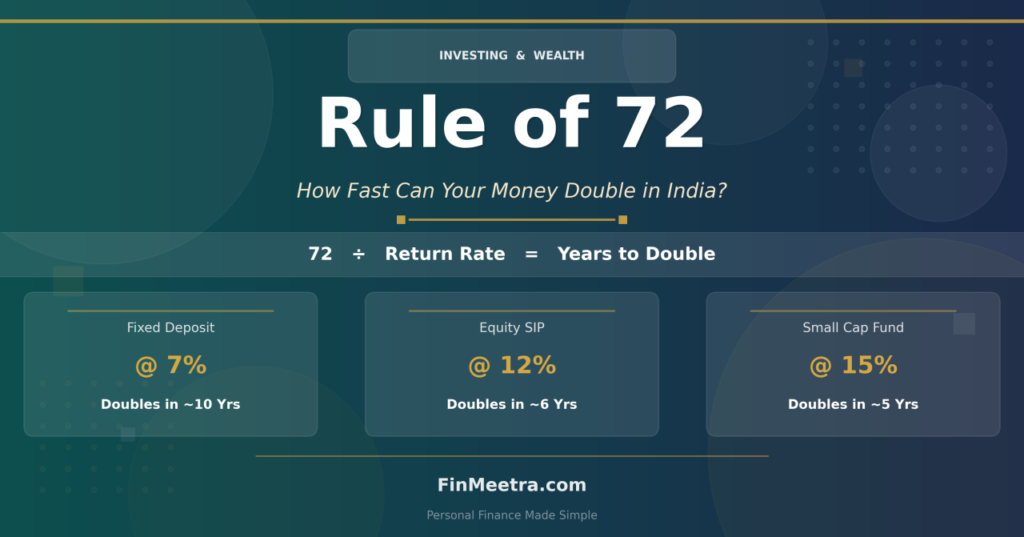

The Formula — Simple Enough for a Chai Break

| 📐 Years to Double Your Money = 72 ÷ Annual Rate of Return (%) OR (in reverse): Required Annual Return (%) = 72 ÷ Years in Which You Want to Double |

Examples:

- FD at 7% → 72 ÷ 7 = ~10.3 years to double

- Equity SIP at 12% → 72 ÷ 12 = 6 years to double

- Savings account at 3.5% → 72 ÷ 3.5 = ~20.5 years to double

No calculator. No spreadsheet. Just one division you can do in your head while sipping chai.

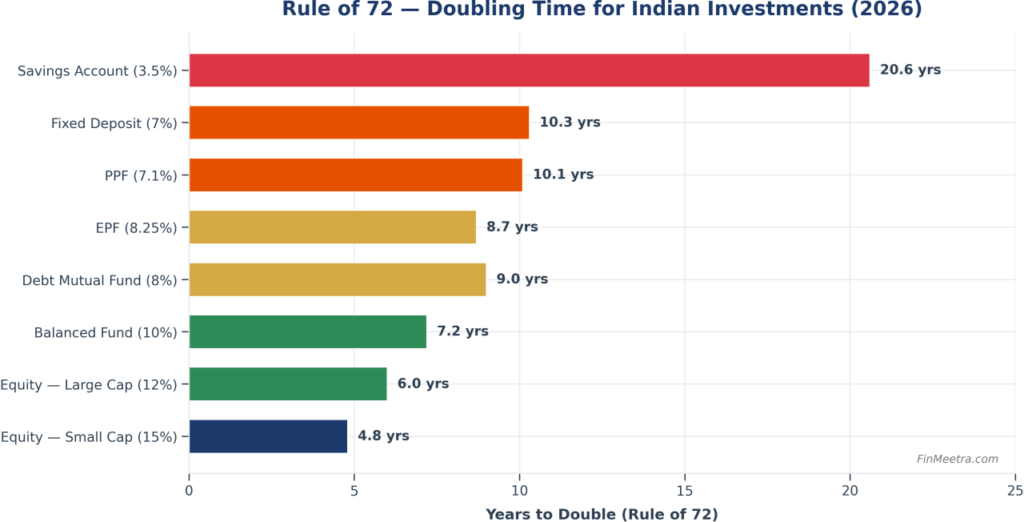

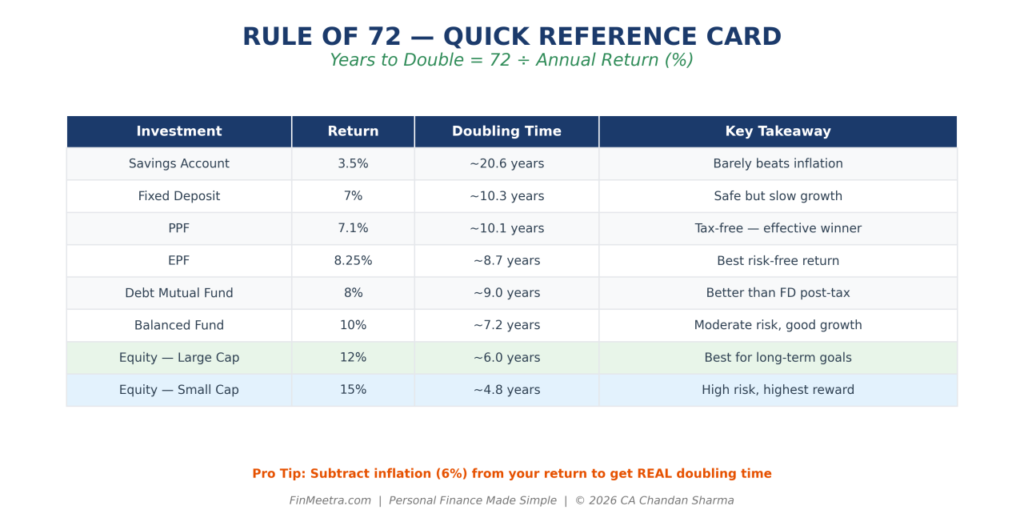

Rule of 72 in Action: Real Indian Investment Comparison

Here is how the Rule of 72 applies to common investment options available to Indians in 2026. This single table can transform how you compare financial products:

| Investment Option | Typical Return (p.a.) | Years to Double (Rule of 72) | Risk Level |

| Savings Account | 3 – 3.5% | 20 – 24 years | ⭐ (Lowest) |

| Fixed Deposit (FD) | 6.5 – 7.25% | 10 – 11 years | ⭐⭐ |

| PPF | 7.1% | ~10.1 years | ⭐⭐ |

| EPF | 8.25% | ~8.7 years | ⭐⭐ |

| Debt Mutual Fund | 7 – 8% | 9 – 10.3 years | ⭐⭐⭐ |

| Balanced / Hybrid Fund | 9 – 10% | 7.2 – 8 years | ⭐⭐⭐ |

| Equity MF (Large Cap) | 10 – 12% | 6 – 7.2 years | ⭐⭐⭐⭐ |

| Equity MF (Small Cap) | 14 – 15% | 4.8 – 5.1 years | ⭐⭐⭐⭐⭐ (Highest) |

| 💡 Key Insight: The difference between 7% (FD) and 12% (Equity SIP) seems like ‘just 5%.’ But through the lens of Rule of 72, it is the difference between your money doubling in 10 years versus 6 years. Over a 30-year career, that ‘small’ gap creates CRORES of difference. |

Real-Life Examples With Amounts

Example 1: Priya — 28, Software Engineer, Bengaluru

Priya receives a ₹3 Lakh annual bonus. She has two options:

Option A: Park it in a Fixed Deposit at 7%

→ 72 ÷ 7 = 10.3 years → ₹3 Lakhs becomes ₹6 Lakhs by age ~38

Option B: Invest in an equity mutual fund averaging 12%

→ 72 ÷ 12 = 6 years → ₹3 Lakhs becomes ₹6 Lakhs by age ~34

But here is where it gets powerful. If Priya stays invested in equity for 24 years (age 52), her ₹3 Lakhs doubles FOUR times:

₹3L → ₹6L → ₹12L → ₹24L → ₹48 Lakhs

Same ₹3 Lakhs in FD for 24 years? It doubles roughly twice:

₹3L → ₹6L → ₹12L (and still needs 2+ more years for the third doubling)

Example 2: Rahul — 35, Small Business Owner, Jaipur

Rahul wants to save ₹50 Lakhs for his daughter’s education by the time she turns 18. She is currently 3 years old, so he has 15 years.

Using Rule of 72 in reverse:

72 ÷ 15 years = ~4.8% minimum return needed to double once.

But Rahul does not just need to double — he needs to grow significantly. If he invests ₹12 Lakhs today in an instrument averaging 12% return:

→ Doubles in 6 years: ₹24 Lakhs (daughter age 9)

→ Doubles again in 6 years: ₹48 Lakhs (daughter age 15)

→ By age 18: approximately ₹68 Lakhs

One lump sum. One smart decision. Rule of 72 helped him see the path clearly.

Rule of 72 in Reverse: What Return Do You Need?

The Rule of 72 is not just about estimating time. Flip it around, and it tells you the return you need to hit your goal in a specific timeframe.

| 📐 Required Return = 72 ÷ Number of Years to Double |

Real scenarios:

- Want to double in 4 years? → 72 ÷ 4 = 18% return needed (aggressive equity / small caps)

- Want to double in 6 years? → 72 ÷ 6 = 12% return needed (equity mutual funds)

- Want to double in 8 years? → 72 ÷ 8 = 9% return needed (balanced/hybrid funds)

- Want to double in 10 years? → 72 ÷ 10 = 7.2% return needed (FD or PPF)

This reverse calculation is incredibly powerful for goal-based planning. Whether it is your child’s education, a house down payment, or retirement — you now know exactly what return profile to target.

The Inflation Trap: Rule of 72 Reveals the Truth

Here is something most people overlook: the Rule of 72 works for inflation too. And the picture is not pretty.

| 🔥 Hot Take: If inflation averages 6% in India — which it roughly has over the past decade — the purchasing power of your money HALVES every 12 years. ₹1 Lakh today → Feels like ₹50,000 in 12 years → Feels like ₹25,000 in 24 years Your FD earning 7% is barely beating inflation by 1%. After tax? You might actually be LOSING money in real terms. The order of financial learning is clear: 1️⃣ Budget your money (50-30-20 Rule) 2️⃣ Protect your money (Emergency Fund) 3️⃣ GROW your money faster than inflation (Rule of 72) |

This is why understanding Rule of 72 is not optional — it is survival. If your money does not double faster than inflation halves its value, you are running on a treadmill going nowhere.

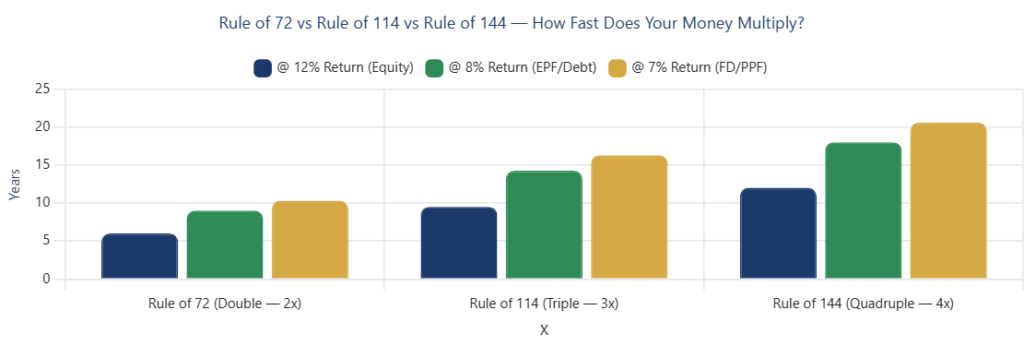

Beyond Doubling: Rule of 114 and Rule of 144

The Rule of 72 has two siblings that are equally powerful:

| Rule | What It Calculates | Formula | Example (at 12% return) |

| Rule of 72 | Time to DOUBLE (2x) | 72 ÷ Rate | 72 ÷ 12 = 6 years |

| Rule of 114 | Time to TRIPLE (3x) | 114 ÷ Rate | 114 ÷ 12 = 9.5 years |

| Rule of 144 | Time to QUADRUPLE (4x) | 144 ÷ Rate | 144 ÷ 12 = 12 years |

So at 12% return, your ₹1 Lakh becomes:

- ₹2 Lakhs in 6 years (Rule of 72)

- ₹3 Lakhs in 9.5 years (Rule of 114)

- ₹4 Lakhs in 12 years (Rule of 144)

| 🎯 Reality Check: At 12% return, your money quadruples in 12 years. At 7% FD rate, it barely doubles in the same period. This is not a marginal difference — this is the difference between financial freedom and financial anxiety. |

5 Practical Ways to Use the Rule of 72 Today

1. Compare Investment Options Instantly

Next time someone offers you a ‘great FD rate’ of 7.5%, do the math: 72 ÷ 7.5 = 9.6 years to double. Compare that with your SIP’s 12% average: 72 ÷ 12 = 6 years. Now you have clarity, not confusion.

2. Set Realistic Financial Goals

Planning for retirement or a child’s education? Use the reverse formula to determine what return you need. If your goal requires doubling in 5 years, you need 72 ÷ 5 = 14.4% — which means you need equity exposure, not FDs.

3. Understand the True Cost of Debt

The Rule of 72 works for debt too. Credit card debt at 36% interest? 72 ÷ 36 = 2 years for your debt to double if unpaid. That ₹50,000 credit card balance becomes ₹1 Lakh in just 2 years. Terrifying, right? This is why emphasised an emergency fund — to avoid high-interest debt.

4. Measure Inflation’s Impact on Your Savings

At 6% inflation: 72 ÷ 6 = 12 years for prices to double. That ₹50 Lakh house will cost ₹1 Crore in 12 years. Your savings need to at least match this pace.

5. Evaluate Business Decisions (For Founders)

If your business grows at 24% annually: 72 ÷ 24 = 3 years to double revenue. This helps founders set realistic milestones and communicate growth potential to investors with a single, compelling number.

3 Common Mistakes When Using the Rule of 72

Mistake #1: Ignoring Tax on Returns

The Problem: Your FD gives 7%, but after 30% tax, your effective return is only ~4.9%. The real doubling time? 72 ÷ 4.9 = 14.7 years — not 10.3.

The Fix: Always calculate using post-tax returns. This is why tax-free instruments like PPF and ELSS are valuable — they give you the full compounding benefit.

Mistake #2: Assuming Fixed Returns for Equity

The Problem: Rule of 72 assumes a constant rate of return. But equity returns fluctuate wildly. Your SIP might give 20% one year and -10% the next.

The Fix: Use long-term average returns (10-15 years) for equity calculations. The 12% average for large cap equity holds well over long horizons in India.

Mistake #3: Forgetting About Inflation

The Problem: Your money doubled! But prices also doubled. You are back to square one.

The Fix: Always subtract inflation from your return before applying Rule of 72. Real return = Nominal return – Inflation rate. If your SIP earns 12% and inflation is 6%, your real return is 6% → 72 ÷ 6 = 12 years for your purchasing power to truly double.

Frequently Asked Questions

Q: What is the Rule of 72 with a simple example?

The Rule of 72 is a mental shortcut to estimate how many years it takes for your money to double. Simply divide 72 by the annual return rate. Example: If you invest in PPF at 7.1%, then 72 ÷ 7.1 = approximately 10.1 years to double your money.

Q: How long does it take to double money in a Fixed Deposit in India?

At current FD rates of 6.5–7.25%, it takes approximately 10–11 years for your money to double. Using Rule of 72: at 7% FD rate, 72 ÷ 7 = 10.3 years. However, after accounting for tax (especially in the 30% bracket), the effective doubling time could be 14–15 years.

Q: Is the Rule of 72 accurate?

Yes, it is remarkably accurate for interest rates between 6% and 10%, which covers most Indian investment products (FDs, PPF, debt funds). For rates outside this range — very high (>15%) or very low (<4%) — the approximation becomes less precise, but still gives a useful ballpark estimate.

Q: What is the difference between Rule of 72, Rule of 114, and Rule of 144?

Rule of 72 estimates time to DOUBLE your money (2x). Rule of 114 estimates time to TRIPLE your money (3x). Rule of 144 estimates time to QUADRUPLE your money (4x). All work the same way: divide the rule number by your annual return rate.

Q: Can I use Rule of 72 for SIP investments?

The Rule of 72 is technically designed for lump sum investments with fixed compounding. For SIPs (where you invest monthly), it gives a rough indication but is not perfectly accurate because each instalment starts compounding at a different time. For precise SIP calculations, use a dedicated SIP calculator. However, for mental estimation and comparison, Rule of 72 is still very useful.

Q: How does Rule of 72 help with inflation?

Divide 72 by the inflation rate to see how quickly prices double. At 6% inflation in India: 72 ÷ 6 = 12 years for the cost of living to double. This means your ₹30,000 monthly expenses today will become ₹60,000 in 12 years. If your investments are not growing faster than inflation, you are actually losing wealth.

Final Thoughts: Your Money Has a Clock — Start Reading It

The Rule of 72 is not just a formula. It is a lens — a way of seeing money that most people never develop. Once you understand it, you will never look at a savings account, an FD, or a mutual fund the same way again.

You will ask better questions: “At this rate, how quickly does my money double?” You will make faster decisions: “FD doubles in 10 years, equity in 6 — the choice is clear for long-term goals.” And you will understand why starting early matters more than starting big.

Here is your action plan for today:

- Pick your top 3 investments — calculate their doubling time using Rule of 72

- Calculate your inflation-adjusted (real) doubling time

- Check if your money is growing fast enough for your biggest financial goal

- If you have not started budgeting yet, read — The 50-30-20 Rule

- If your emergency fund is not in place, read — The Complete Emergency Fund Guide

- Share this blog with someone who still thinks FDs are the ‘safest’ way to grow wealth

| 🚀 Start applying the Rule of 72 today. Your money is either working for you — or against you. Now you have the formula to know which. 📖 Missed the earlier Updates? → How to Create a Monthly Budget (50-30-20 Rule) → The Complete Emergency Fund Guide: How Much You Really Need in 2026 |

Pingback: Free SIP Calculator Excel: 8-Sheet Premium Toolkit (2026) | FinMeetra