I will never the forget the first time i checked my bank balance after a “normal” month. No big purchases, no vacations, no emergencies, just regular life.

And somehow, 80% of my salary had already vanished. Rent, food, Swiggy orders i didn’t need, a subscription i forgot to cancel and then about 15 small UPI payments that couldn’t even remember making.

Sound Familiar?

Here’s what i have learnt since then. The problem was never my salary. The problem was i had no system. I was earning money and spending money but i had zero plan for what should go where.

That’s when i discovered the monthly Budget rule of 50-30-20 and honestly, it changed everything. Not because it’s some complicated financial formula but because it’s stupidly simple. Anyone can follow it. You don’t need an excel course or a financial degree. Just a salary and 10 min of your time.

Let me walk you through it.

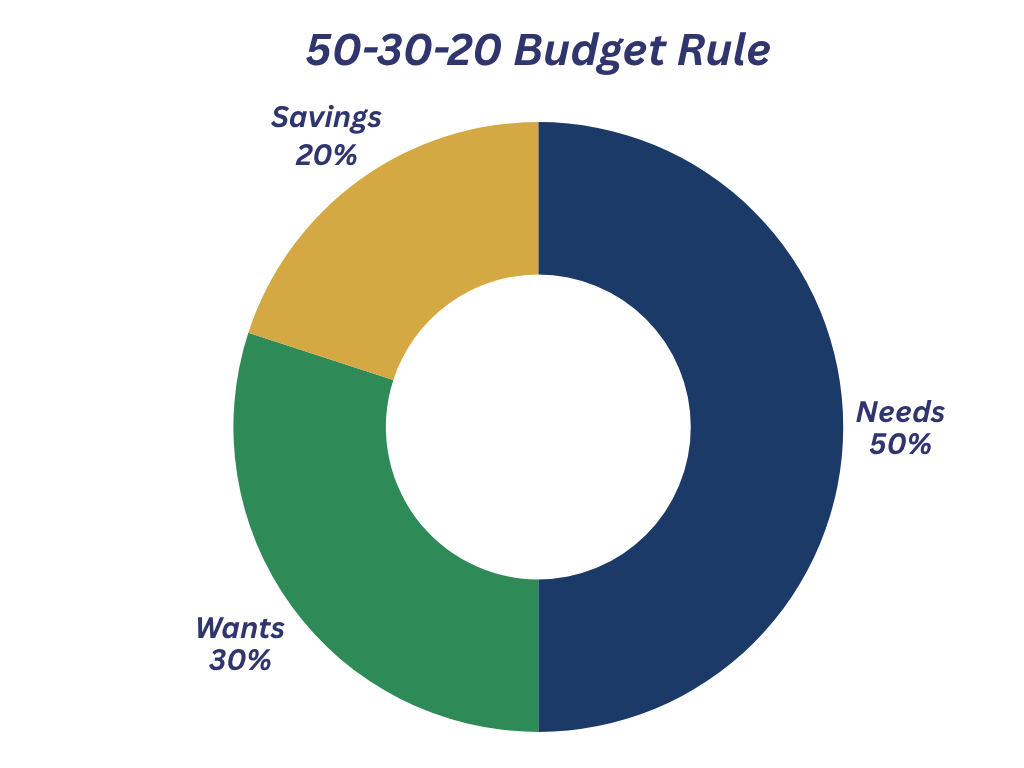

What Exactly is the 50-30-20 Rule?

The 50-30-20 rule is a budgeting framework that divides your take home salary (In-hand salary, after tax) into three simple buckets.

- 50% – Needs – Thing’s you can’t avoid

- 30% – Wants – Thing’s you enjoy but can live without

- 20% – Savings – Money you set aside before spending anything else

That’s it. No heavy categories, No colour spreadsheets. Just three buckets.

This rule was first made popular by Elizabeth Warren in her book “All Your Worth”. But the beauty of it is that it works everywhere. Whether your in-hand salary is 25,000 or 1,50,000 the percentage stays the same.

Before you start – Know your In-Hand Salary

The 50-30-20 rule works on your in-hand salary and not on your CTC or Gross Salary. The actual amount that gets credited to your bank account every month.

If your offer letter says CTC 6,00,000 per annum, your in-hand per month might only be 42,000 to 45,000 after PF, tax and any other deductions. Use THAT number.

‘Quick Check: Open your bank statement, find last month’s salary credit. That’s your number.

The 50-30-20 Rule with Real Indian Salaries

Enough theories, let see this in practical

| In-Hand Salary | 50% Needs | 30% Wants | 20% Savings |

| 20,000 | 10,000 | 6,000 | 4,000 |

| 30,000 | 15,000 | 9,000 | 6,000 |

| 50,000 | 25,000 | 15,000 | 10,000 |

| 75,000 | 37,500 | 22,500 | 15,000 |

| 1,00,000 | 50,000 | 30,000 | 20,000 |

Look at the 20,000 row. Even at that salary, 4,000 goes to savings. That’s 48,000 a year. It might not sound like much but that habit is what seperates people who are always broke from people who slowly build wealth.

The 50% – Needs (Non-Negotiable Expenses)

These are expenses you absolutely cannot skip. If you stop paying them, your life falls apart.

Simple test: “Will i face a serious problem if i don’t pay this for 2 months?” If yes, it’s a Need.

What Counts as Needs:

- Rent or Home loan EMI

- Groceries and Household essentials (Rice, Dal, Oil, Milk etc., but does not include Zomato/Swiggy)

- Electricity, Water, Cooking Gas bill

- Mobile Phone and Internal Bill

- Transportation – Fuel, Metro Pass or Bus Fare

- Health Insurance Premium

- Term Life Insurance Presmium

- Minimum Loan EMIs (Education, Car, Personal loan etc.,)

- Children’s School Fees

- Essential Medicines and Health Care

What Does Not Count as Need:

- Netflix, Hotstar, Spotify etc., – Want

- Eating out at restaurants – Want

- Gym Membership – Want

- That “essential” new phone – Want

If your needs exceed 50%, don’t panic. That’s common in Mumbai, Bangalore, Delhi or Top tier cities where rent alone can be 30%-40% of your in-hand salary. Adjust to 60-20-2- rule but make sure your savings component should not come down to 15%.

The 30% – Wants (The Fun Money)

This is where most people mess up. Not because they spend too much on wants but because they confuse wnats with needs.

Quick test: “I really want this” vs “I will literally suffer without this”, if it’s the 1st one, it’s a want.

What Count as Want:

- Eating out – Restaurant, Swiggy, Zomato etc.,

- Shopping – Clothes, Gadgets, Accesories beyond basics

- Entertainment – Movies, OTT Subscription, Concerts

- Gym membership or fitness classes

- Weekend trips and Short vacations

- That fancy coffee from the cafe near your office

- Upgrading your phone when old one works fine

- Hobbies – Gaming, Books

I want to be very clear, the 30% for wants is NOT a “waste” category. This is the money that makes life enjoyable. Budgeting isn’t about punishing yourself. It’s about spending intentionally on things that actually makes you happy, instead of randomly bleeding money on stuff you don’t even remember buying.

The goal isn’t 0 wants. The goal is the wants you actually care about.

Trick That Worked for Me

I transfer my waste budget to a separate bank account at the start of each month. When that account hits zero, i stop spending on wants. No guilt when I’m spending from it. No overspending when it’s empty, SIMPLE.

The 20% – Savings (Pay Yourself First)

This is the most important bucket and i’m going to keep this section deliberately simple because the WHERE to invest question deserves its own detailed post.

Right now, let’s focus on the habbit because the habbit matter 100X more than the instrument.

The One Rule: Pay Yourself First

Most people spend first and “save whatever is left”. Here is the problem – There’s never anything left.

Flip it around

Salary Credited —- Immediately move 20% to a separate account —- Sepnd from whatever remains.

That one sentence is more than any investment tip i can give you. Set up an automatic transfer on salary day.

That’s it. Dont overthink this. DON’T research mutual fund, SIP or any other investment ideas right now. Focus on the habit, 20% out every month on salary day, no exceptions

The Bottom Line

The 50-30-20 rule won’t make you rich overnight. No budget will.

But it does something even more powerful, it gives you CONTROL. It takes money from being this vague stressful things to being something you actually understand and manage.

You don’t need a CA to tell you this, You just need to start. Open your bank account right now, Calculate your Rule and Set up auto transfer.

That’s it. You just started budgeting.

Your Future Self will Thank you for it.

Pingback: Rule of 72 - How Fast Can Your Money Double | FinMeetra

Pingback: How to Start Your First SIP in India — Complete 2026 Guide | FinMeetra

Pingback: SIP vs Lump Sum: Which Investment Strategy Wins? 2026 | FinMeetra

Pingback: How to Choose the Right Mutual Fund: 7-Filter Framework (2026) | FinMeetra