Table of Contents

The Day My Colleague’s Life Changed

(And Why I Started Taking This Seriously)

A few years ago, a close colleague of mine — someone who earned well, drove a nice car, and seemed to have it all figured out — got laid off without warning. No severance. No notice.

Within two weeks, the cracks appeared. Credit card bills started piling up. An EMI bounce happened. Then a frantic call to family asking for money.

The worst part? This person earned over 1 Lakh a month. But savings? Almost zero. Everything went into SIPs, stocks, and lifestyle.

Here’s what hit me hardest: it took just 45 days for someone earning a six-figure salary to go from ‘comfortable’ to ‘desperate.’

That day, I promised myself I’d never be in that situation. And I want to make sure you aren’t either.

This guide isn’t written by a bank trying to sell you a product. It’s written by someone who has seen — up close — what happens when you don’t have a financial safety net. Let’s build yours today.

What Is an Emergency Fund — And What It’s NOT

An emergency fund is a dedicated pool of money, kept in safe and easily accessible instruments, meant exclusively for life’s unexpected financial shocks. Think of it as your financial first-aid kit — boring, unsexy, but absolutely life-saving when you need it.

It IS for:

✅ Job loss or sudden income disruption

✅ Medical emergencies not fully covered by insurance

✅ Urgent home or vehicle repairs

✅ Family emergencies or unexpected travel

✅ Gap between jobs (especially in today’s market)

It is NOT for:

❌ A new phone or gadget upgrade

❌ That Goa trip you’ve been planning

❌ A ‘great stock tip’ your friend shared

❌ Wedding shopping or festival expenses (these are planned — save separately!)

❌ Everyday bills and rent

| 💡 Simple Rule: If you saw it coming more than 30 days ago, it’s NOT an emergency. Plan for it separately. |

Why You Need One in 2026 (More Than Ever Before)

Let’s be real — 2026 isn’t 2015. The financial landscape in India has changed dramatically. Here’s why an emergency fund is no longer optional:

- Tech Layoffs Are Real: From startups to large IT companies, job cuts have become a recurring headline. AI is reshaping entire departments. Even ‘stable’ jobs aren’t guaranteed anymore.

- Medical Inflation Is Brutal: Healthcare costs in India are rising at 14-15% annually. Even with corporate insurance, consumables, room upgrades, and post-care expenses often come out of pocket. One hospitalization can cost 2-5 Lakhs easily.

- The Sandwich Generation Pressure: If you’re in your 30s-40s, you’re likely supporting both aging parents and growing children. That’s a double financial burden with zero margin for error.

- AI & Automation Disruption: Roles that felt safe 3 years ago are being automated. The transition period between jobs is getting longer as people upskill. You need a financial bridge.

- Freelance & Gig Economy Growth: More Indians are freelancing than ever. With irregular income comes the absolute necessity of a larger emergency buffer.

How Much Do You Really Need? The 3-6-12 Rule

Forget the generic ‘save 3 months’ advice your grandfather gave you. In 2026, the right number depends entirely on your life situation. Here’s the framework that actually works:

| Your Situation | Recommended Coverage | Why This Much? |

| Stable salaried (Govt/MNC) | 3-4 months | Predictable income, notice period, employer insurance |

| Private sector / Startup employee | 6 months | Higher layoff risk, competitive job market |

| Freelancer / Consultant / Gig worker | 9-12 months | Irregular income, no severance or notice period |

| Business owner | 12 months | Business cycles directly affect personal income |

| Single income household with dependents | 6-9 months | No backup income if earner loses job |

| Dual income, no kids | 3-4 months | Two income sources provide natural buffer |

| ⚡ Pro Tip: Base your emergency fund on your EXPENSES, not your SALARY. Your salary includes taxes, investments, and lifestyle spending. Your survival number is much lower — and that’s what matters in a crisis. |

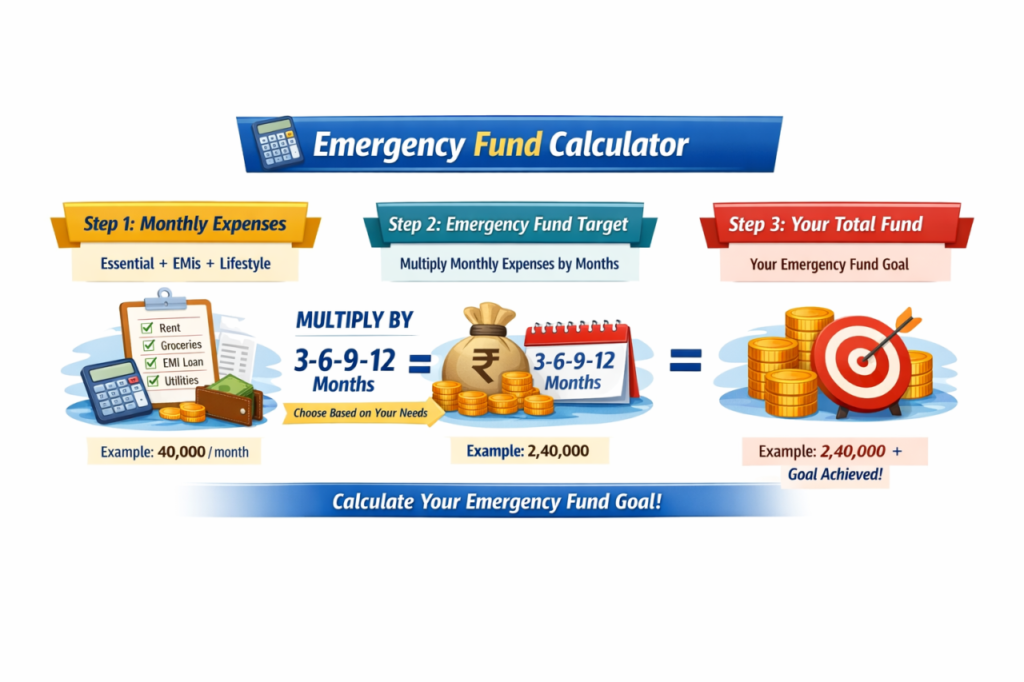

How to Calculate Your Exact Number (With Real Examples)

The Formula:

| 📐 Emergency Fund Target = Monthly Essential Expenses × Recommended Months Essential Expenses = Rent/EMI + Groceries + Utilities + Insurance Premiums + Loan EMIs + Transport + Medical + School Fees (if any) |

Real Example 1: Young Professional (Single, Metro City)

| Expense Category | Monthly Amount |

| Rent | 12,000 |

| Groceries & Food | 6,000 |

| Utilities (Electricity, Internet, Phone) | 3,000 |

| Transport (Metro/Fuel) | 3,000 |

| Insurance Premium | 2,000 |

| Miscellaneous Essentials | 4,000 |

| TOTAL Monthly Essentials | 30,000 |

→ For a private sector employee: 30,000 × 6 = 1,80,000 (1.8 Lakhs)

→ For a freelancer: 30,000 × 9 = 2,70,000 (2.7 Lakhs)

Real Example 2: Family (Married, 1 Child, Tier-1 City)

| Expense Category | Monthly Amount |

| Home Loan EMI | 22,000 |

| Groceries & Household | 10,000 |

| Utilities | 5,000 |

| Child’s School Fees | 8,000 |

| Insurance Premiums | 5,000 |

| Transport | 5,000 |

| Medical (Regular) | 3,000 |

| Domestic Help | 2,000 |

| TOTAL Monthly Essentials | 60,000 |

→ Single income household: 60,000 × 9 = 5,40,000 (5.4 Lakhs)

→ Dual income household: 60,000 × 4 = 2,40,000 (2.4 Lakhs)

Where to Park Your Emergency Fund in 2026

This is where most people get it wrong. Your emergency fund is NOT an investment. You’re optimizing for safety and speed of access — not returns. Here’s what works in India right now:

| Option | Safety | Liquidity | Returns (2026) | Best For |

| Savings Account | ⭐⭐⭐⭐⭐ | Instant | 3 – 3.5% | First 1-2 months of expenses |

| Fixed Deposit (Short-term) | ⭐⭐⭐⭐⭐ | 1-2 days (penalty on early withdrawal) | 6 – 7.25% | 2-3 months portion |

| Liquid Mutual Fund | ⭐⭐⭐⭐ | T+1 day (next business day) | 6 – 7% | Bulk of the fund (3+ months) |

| Sweep FD | ⭐⭐⭐⭐⭐ | Same day | 5.5 – 6.5% | Good hybrid option |

Where NOT to Keep Your Emergency Fund:

🚫 Stocks or equity mutual funds (too volatile — you might need to sell at a loss)

🚫 PPF or NPS (locked in — defeats the purpose)

🚫 Crypto (not your safety net, ever)

🚫 Gold (not liquid enough when you need cash at 2 AM for a hospital bill)

The Smart 2-Bucket Strategy

Here’s the approach I personally use, and it’s recommended by most India-focused financial planners. Instead of dumping everything in one place, split your emergency fund into two buckets:

🪣 Bucket 1 — Instant Access (1-2 Months of Expenses)

Keep this in a separate savings account (not your salary account). This is your ‘break glass in emergency’ money. You can access it via UPI, debit card, or ATM within seconds. No questions asked.

Pro tip: Open this account in a different bank than your salary account. Don’t link it to any UPI app you use for daily spending. Make it invisible until you need it.

🪣 Bucket 2 — Growth Layer (Remaining 4-10 Months)

Split this between a liquid mutual fund (70%) and a short-term FD (30%). The liquid fund gives you T+1 access with better returns than a savings account. The FD provides rock-solid safety.

This way, your money isn’t sitting idle earning 3% — it’s working at 6-7% while still being accessible within 24-48 hours when needed.

| 💡 Example: If your total emergency fund target is 3 Lakhs: • Bucket 1 (Savings Account): 60,000 (2 months) • Bucket 2 — Liquid Fund: 1,68,000 (70% of remaining) • Bucket 2 — Short-term FD: 72,000 (30% of remaining) |

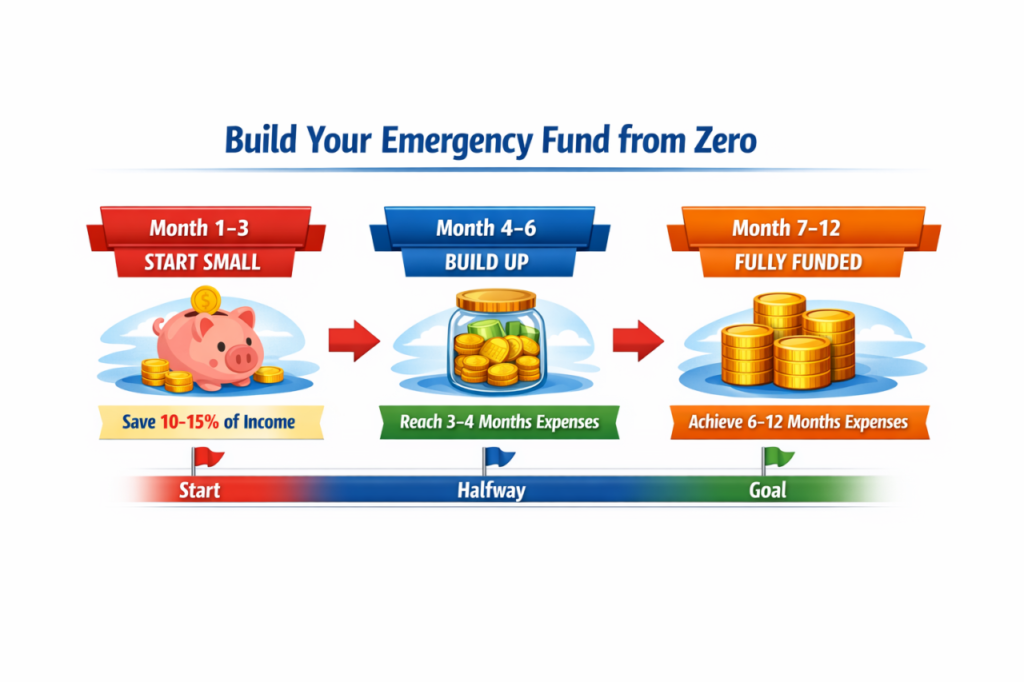

Step-by-Step: Build Your Emergency Fund from Zero

Feeling overwhelmed by the target number? Don’t be. You don’t need to build it overnight. Here’s a practical, month-by-month plan that actually works:

Step 1: Calculate Your Monthly Essential Expenses

Use the formula above. Be honest — include only what you MUST pay even if you lose your income tomorrow. Not Netflix. Not Zomato. The real non-negotiables.

Step 2: Set Your Target

Multiply your monthly essentials by the recommended months from the 3-6-12 rule. Write this number down. Stick it on your mirror. Make it real.

Step 3: Open a Separate Account

Go to any bank (IDFC First, Axis, Kotak — all offer good digital savings accounts). Open an account specifically for your emergency fund. No debit card. No UPI for daily use.

Step 4: Automate a Monthly Transfer

Set up an auto-debit of 10-20% of your take-home salary on the 1st of every month. Treat it like an EMI you can’t skip. Pay yourself first — before the world takes its share.

Step 5: Scale Up Progressively

Month 1-3: Build Bucket 1 (savings account). Month 4+: Start routing surplus into a liquid fund (Bucket 2). Use any bonus, tax refund, or windfall to fast-track the fund.

Sample Monthly Savings Plan

| Monthly Savings | 6 Months | 12 Months | 18 Months | 24 Months |

| 5,000 / month | 30,000 | 60,000 | 90,000 | 1,20,000 |

| 10,000 / month | 60,000 | 1,20,000 | 1,80,000 | 2,40,000 |

| 15,000 / month | 90,000 | 1,80,000 | 2,70,000 | 3,60,000 |

| 20,000 / month | 1,20,000 | 2,40,000 | 3,60,000 | 4,80,000 |

| 🎯 Reality Check: Even saving 5,000 a month gets you to 1.2 Lakhs in 2 years. That’s a solid 4-month buffer for someone with 30,000 monthly expenses. Start small. Start now. |

5 Emergency Fund Mistakes That Cost You Money

Mistake #1: Keeping it in your salary account

The Problem: Your brain treats it as spending money. Every Swiggy order, every ‘small’ purchase slowly erodes it. Studies show 25-30% annual depletion when emergency funds sit in everyday accounts.

The Fix: Open a separate account. Don’t link a debit card. Make it invisible.

Mistake #2: Locking it in a 5-year FD

The Problem: Great returns on paper. But when your mother needs emergency surgery at 11 PM, that locked FD is useless. Early withdrawal means penalties and 3-day waits.

The Fix: Use liquid funds + short-term FDs (3-6 month tenure) instead.

Mistake #3: Not starting because the target feels ‘too big’

The Problem: “I need 5 Lakhs? That’s impossible, I’ll start later.” Later never comes. And then the emergency does.

The Fix: Start with 1,000 a month. Something is infinitely better than nothing.

Mistake #4: Using it for non-emergencies

The Problem: That ‘amazing deal’ on a phone? Not an emergency. Your friend’s destination wedding? Not an emergency. A planned expense is NOT an emergency — no matter how urgent it feels.

The Fix: Ask yourself: ‘Did I know about this 30 days ago?’ If yes → it’s not an emergency.

Mistake #5: Not replenishing after use

The Problem: You used your emergency fund for a medical bill. Great — that’s exactly what it’s for. But then you forgot to rebuild it. Now you’re exposed again.

The Fix: After any withdrawal, make rebuilding the fund your #1 financial priority before any other goal.

Emergency Fund vs Investing — Which Comes First?

I hear this all the time: “But if I put money in an emergency fund, I’ll miss out on SIP returns!”

Let me be brutally honest:

| 🔥 Hot Take: An emergency fund earning 6% will ALWAYS outperform a SIP you were forced to redeem at a 30% loss during a market crash because you had no safety net. The order is non-negotiable: 1️⃣ Health Insurance → 2️⃣ Emergency Fund (at least 3 months) → 3️⃣ Then start SIPs and investments Your SIP can recover from being delayed by 6 months. Your finances cannot recover from a crisis without a buffer. |

Once your emergency fund is fully built, that’s when the real wealth-building begins. And if you’re looking for a smart, low-risk way to move a lump sum into mutual funds, check out our guide on Systematic Transfer Plans (STP) — it’s a game-changer for new investors who don’t want to time the market.

| 📖 Related Read: Master Your Finances with Monthly Budget Rule of 50-30-20 Concept: Plan you In-Hand Monthly Salary – Save money by calssifying your actual Wants and Needs |

Frequently Asked Questions

Q: How much emergency fund do I need for a 50,000 salary?

Don’t calculate based on salary — calculate based on essential expenses. If your monthly essentials are 30,000 and you’re a salaried employee, you need 1.8 Lakhs to 3.6 Lakhs (6-12 months). If you’re a freelancer, aim for 2.7 to 3.6 Lakhs (9-12 months).

Q: Is 1 Lakh enough for an emergency fund?

It depends on your monthly expenses. If your essentials are 25,000 per month, 1 Lakh covers 4 months — which is a decent start for someone with a stable salaried job. But if you have dependents or an unstable income, you’ll need more. Start with 1 Lakh and keep building.

Q: Where should I keep my emergency fund in India?

Use the 2-bucket strategy: Keep 1-2 months in a separate savings account for instant access. Park the remaining in a mix of liquid mutual funds (70%) and short-term FDs (30%) for better returns while maintaining safety and liquidity.

Q: Should I build an emergency fund or pay off debt first?

Build a starter emergency fund of 1 month’s expenses first. Then aggressively pay off high-interest debt (credit cards, personal loans). Once high-interest debt is cleared, build your full emergency fund. This prevents you from falling back into debt during an emergency while you’re paying off existing debt.

Q: Can I use liquid mutual funds for my emergency fund?

Yes — liquid mutual funds are one of the best options for the bulk of your emergency fund in India. They offer T+1 redemption (money in your account next business day), returns of 6-7% annually, and are much more efficient than a savings account earning 3-3.5%.

Q: How long does it take to build a full emergency fund?

At 10,000 per month savings, you can build a 1.8 Lakh fund (6 months at 30,000 expenses) in about 18 months. Fast-track it by redirecting bonuses, tax refunds, and any windfall income. The key is to start now — even 3,000 per month adds up to 36,000 in a year, which is at least one month’s buffer.

Final Thoughts: Your Safety Net Starts Today

Look, I know emergency funds aren’t exciting. Nobody posts Instagram stories about their liquid fund balance. Nobody brags about their separate savings account at dinner parties.

But here’s what I’ve learned from watching real people go through real financial crises:

The people who sleep well at night aren’t the ones with the highest SIP returns. They’re the ones who know — with absolute certainty — that if life throws a curveball tomorrow, they can handle it without panic, without debt, and without selling their investments at a loss.

That confidence is priceless. And it starts with a simple, boring emergency fund.

So here’s your action plan for today:

- Calculate your monthly essential expenses (use the tables above)

- Pick your target using the 3-6-12 rule

- Open a separate savings account (takes 10 minutes online)

- Set up an auto-transfer for the 1st of next month

- Bookmark this guide and come back in 3 months to check your progress

| 🚀 Start building your emergency fund today. Your future self will thank you. |

Pingback: Rule of 72 - How Fast Can Your Money Double | FinMeetra

Pingback: SIP vs Lump Sum: Which Investment Strategy Wins? 2026 | FinMeetra